On January 20, 2022, on the website of the Court of Justice of the European Union (CJEU) the opinion of Advocate General Collins in Case C- 572/20 ACC Silicones Ltd versus Bundeszentralamt für Steuern (ECLI:EU:C:2022:48), was published.

Introduction

This request for a preliminary ruling concerns the compatibility, with the rules governing the free movement of capital, of the conditions under which German tax legislation permits non-resident companies to obtain the reimbursement of a withholding tax on income from capital consisting of dividends from minority shareholdings in companies established in Germany.

The request arises in the context of a challenge by ACC Silicones Ltd to the refusal by the Bundeszentralamt für Steuern (Federal Central Tax Office, Germany) to allow claims for the reimbursement of that tax, which had been withheld and paid for the years 2006 to 2008 inclusive.

The request follows on from the judgment of 20 October 2011, Commission v Germany (C‑284/09, EU:C:2011:670). In that judgment the Court ruled that, by taxing dividends distributed to non-resident companies where the threshold for a parent company’s holding in the capital of its subsidiary laid down in Article 3(1) of Council Directive 90/435/EEC of 23 July 1990 on the common system of taxation applicable in the case of parent companies and subsidiaries of different Member States, as amended by Directive 2003/123/EC, is not reached, more heavily in economic terms than dividends distributed to resident companies, the Federal Republic of Germany had failed to fulfil its obligations under Article 56(1) EC and Article 40 of the Agreement on the European Economic Area (‘the EEA Agreement’). In order to comply with that judgment, in March 2013, the German legislature enacted, with retroactive effect, Paragraph 32(5) of the Körperschaftsteuergesetz (Law on corporation tax, ‘the KStG’), which provisions fall to be considered in the context of this request for preliminary ruling.

II. Legal context

A. European Union law

4. Article 3(1) of Directive 90/435 provides:

‘For the purposes of applying this Directive:

(a) the status of parent company shall be attributed at least to any company of a Member State which fulfils the conditions set out in Article 2 and has a minimum holding of 20% in the capital of a company of another Member State fulfilling the same conditions;

…

from 1 January 2007 the minimum holding percentage shall be 15%;

from 1 January 2009 the minimum holding percentage shall be 10%;

…’

B. German law

5. The German system of taxation of income from capital is laid down in the Einkommensteuergesetz (Law on income tax, ‘the EStG’), in conjunction, as regards the taxation of legal persons, with the KStG.

6. Point 1 of Paragraph 20(1) of the EStG stipulates that income from capital includes shares of profits (dividends).

7. Point 1 of the first sentence of Paragraph 43(1) of the EStG provides that, in the case, inter alia, of income from capital within the meaning of point 1 of Paragraph 20(1) of the EStG, ‘income tax is levied by deduction from the income from capital (tax on income from capital)’.

8. Under the first sentence of Paragraph 8b(1) of the KStG, relating to shareholdings in other companies and associations, earnings received within the meaning, inter alia, of point 1 of Paragraph 20(1) of the EStG are not to be taken into account for the purpose of determining income and are therefore not subject to corporation tax.

9. As regards the taxation of dividends distributed to a company whose registered office is in Germany, it is apparent from the combined provisions of the first sentence of Paragraph 31(1) of the KStG and point 2 of Paragraph 36(2) of the EStG that the tax on income from capital which has been levied by way of a withholding tax is offset in full against the corporation tax payable by that company and, where appropriate, may be reimbursed to it. The set-off (and reimbursement, if any) of the tax presupposes that the tax has been withheld and paid, which must be proved by the submission of an administrative certificate, in accordance with Paragraph 45a(2) or (3) of the EStG.

10. As regards the taxation of dividends distributed to a company whose registered office is not in Germany, Paragraph 32(5) of the KStG lays down a number of conditions governing the reimbursement of tax on income from capital. These include certain obligations to furnish proof and certificates. That provision reads as follows:

‘(5) [First sentence] Where the corporation tax owed by the creditor on income from capital within the meaning of point 1 of Paragraph 20(1) of [the EStG] has been definitively disposed of in accordance with subparagraph 1 [hereof], the tax on income from capital which has been withheld and paid shall, on application, be reimbursed to the creditor of the income from capital in accordance with point 2 of Paragraph 36(2) of [the EStG], where

1. the creditor of the income from capital is a company subject to limited tax liability as provided for in Paragraph 2(1), which

(a) is also a company within the meaning of Article 54 of the Treaty on the Functioning of the European Union or Article 34 of the [EEA Agreement],

(b) has its registered office and centre of effective management within the territory of a Member State of the European Union or a State to which the [EEA Agreement] is applicable,

(c) is subject, in the State of its centre of effective management, to non-optional, unlimited tax liability comparable to that referred to in Paragraph 1, and is not exempt therefrom, and

2. the creditor has a direct holding in the initial capital or share capital of the debtor of the income from capital and does not meet the minimum participation threshold laid down in Paragraph 43b(2) of [the EStG].

[Second sentence] Sentence 1 shall apply only in so far as

1. reimbursement of the tax on income from capital in question is not available under any other provision,

2. the income from capital would not be taken into account in the calculation of income, in accordance with Paragraph 8b(1),

3. the income from capital is not attributed, under provisions in another country, to any person who would not be entitled to reimbursement pursuant to this subparagraph if he or she were to receive the income from capital directly,

4. a right to full or partial reimbursement of the tax on income from capital would not be excluded if Paragraph 50d(3) of [the EStG] were applied mutatis mutandis, and

5. the creditor or a shareholder having a direct or indirect equity holding in the creditor cannot offset the tax on income from capital or deduct it as an operating cost or as work-related outgoings; the possibility of carrying forward a set-off shall be treated as a set-off.

[Third sentence] The creditor of the income from capital shall provide proof of compliance with the conditions of reimbursement. [Fourth sentence] In particular, he or she shall prove, by way of a certificate from the tax authorities of his or her country of residence, that he or she is regarded as being resident for tax purposes in that country, is subject to unlimited corporation tax liability there, is not exempt from corporation tax and is the actual recipient of the income from capital. [Fifth sentence] The certificate from the foreign tax administration shall show that the German tax on income from capital cannot be offset, deducted or carried forward and that no set-off, deduction or carry-forward has actually taken place either. [Sixth sentence] The tax on income from capital shall be reimbursed in relation to all income from capital received in a calendar year within the meaning of the first sentence on the basis of an exemption notice as provided for in the third sentence of Paragraph 155(1) of the Abgabenordnung [(German Tax Code)].’

C. Convention for the avoidance of double taxation concluded between Germany and the United Kingdom

11. On 26 November 1964, the Federal Republic of Germany concluded with the United Kingdom of Great Britain and Northern Ireland a convention for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and fortune (‘the Convention’).

12. Article XVIII(1)(a) of the Convention is worded as follows:

‘(1) Subject to the provisions of the law of the United Kingdom regarding the allowance as a credit against United Kingdom tax of tax payable in a territory outside the United Kingdom (which shall not affect the general principle hereof):

(a) Federal Republic tax payable under the laws of the Federal Republic and in accordance with this Convention, whether directly or by deduction, on profits, income or chargeable gains from sources within the Federal Republic (excluding in the case of a dividend, tax payable in respect of the profits out of which the dividend is paid) shall be allowed as a credit against any United Kingdom tax computed by reference to the same profits, income or chargeable gains by reference to which the Federal Republic tax is computed’.

The dispute in the main proceedings and the questions referred for a preliminary ruling

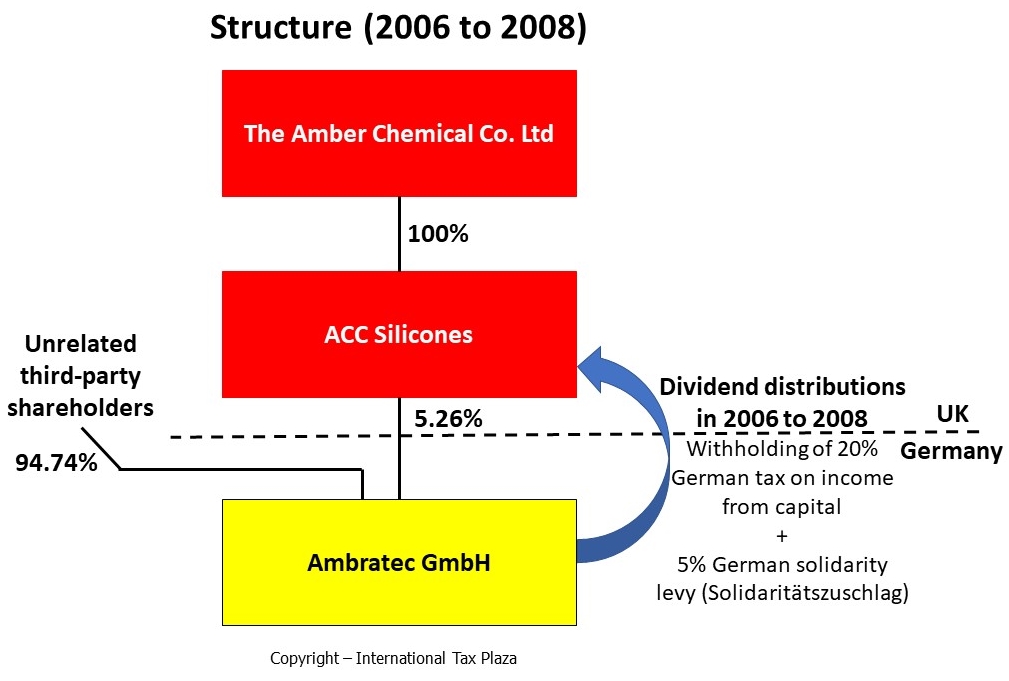

13. ACC Silicones is a company established in the United Kingdom. It is wholly owned by The Amber Chemical Co. Ltd, a company which is also established in the United Kingdom. In the years at issue (2006 to 2008), ACC Silicones had a 5.26% equity holding in the nominal capital of Ambratec GmbH, a company established in Germany. Ambratec distributed dividends to ACC Silicones, on which the tax on income from capital at a rate of 20%, plus the solidarity levy (Solidaritätszuschlag) at a rate of 5.5%, was withheld.

14. By applications of 29 December 2009, each divided in two parts, ACC Silicones requested reimbursement of the amounts paid in respect of withholding tax for each of the years at issue. In the first part, relying on the combined provisions of Paragraph 50d(1) of the EStG and of Article VI(1) of the Convention, it asked that the rate of the tax charged on the dividends at issue be limited to 15%. In the second part, relying on the fundamental freedoms guaranteed by the EC Treaty and the TFEU, it sought reimbursement of the balance of the tax withheld.

15. By decision of 7 October 2010, the Federal Central Tax Office granted the first part of the applications for reimbursement.

16. By contrast, by two decisions of 8 June 2015, the Federal Central Tax Office rejected the second part of those applications on the ground that the conditions laid down in Paragraph 32(5) of the KStG to obtain reimbursement of the tax on income from capital had not been fulfilled. Following the dismissal of its complaints against those decisions, ACC Silicones brought an action to challenge them before the referring court, the Finanzgericht Köln (Finance Court, Cologne, Germany), arguing that it satisfied all the requisite conditions and that it had provided all of the evidence required for that purpose.

17. According to the referring court, ACC Silicones fulfils all the conditions for obtaining reimbursement of the taxes paid, with the exception of that laid down in point 5 of the second sentence of Paragraph 32(5) of the KStG. The referring court states that it follows from that provision that reimbursement is granted only where the disadvantage to foreign dividend recipients as compared with domestic dividend recipients cannot be equalised by set-off, deduction from the basis of assessment or carry-forward of the set-off in the other country.

18. The referring court observes that, pursuant to the fifth sentence of Paragraph 32(5) of the KStG, ACC Silicones is required to prove that the condition laid down in point 5 of the second sentence of Paragraph 32(5) of the KStG is met by submitting a certificate from the tax authorities of its country of residence stating that the German tax on income from capital cannot be offset, deducted or carried forward and that no set-off, deduction or carry-forward has actually taken place either. The referring court takes the view that certificates from foreign tax authorities are to be submitted in respect of both the creditor of the income from capital, that is to say, ACC Silicones, and all shareholders with a direct or indirect equity holding in the creditor.

19. The referring court considers that, in the case at issue, it is not possible to determine whether the condition laid down in point 5 of the second sentence of Paragraph 32(5) of the KStG is met. Indeed, it is not readily apparent exactly how tax on income from capital received by The Amber Chemical Co. or by its shareholders is treated. The evidence submitted by ACC Silicones fails to establish that none of its direct or indirect shareholders offset the withheld tax on income from capital or took it into account for tax reduction purposes, and also does not constitute a foreign certificate within the meaning of the fifth sentence of Paragraph 32(5) of the KStG.

20. In those circumstances, the referring court has doubts as to whether the conditions laid down in point 5 of the second sentence of Paragraph 32(5) and in the fifth sentence of Paragraph 32(5) of the KStG are compatible with Articles 63 and 65 TFEU as well as with the principles of proportionality and effectiveness.

21. In the first place, the referring court queries whether the fact that reimbursement of withheld tax on income from capital to companies resident abroad that have an equity holding of less than 10% or 15% in a resident company is subject to stricter conditions than reimbursement of that tax to resident companies that have an equivalent equity holding in a resident company is contrary to Article 63 TFEU. Indeed, under point 5 of the second sentence of Paragraph 32(5) of the KStG, withheld tax is reimbursed to foreign companies only if they, or their direct or indirect shareholders, cannot offset it or deduct it as an operating cost or as work-related outgoings. The referring court also points out that the requirement, laid down in the fifth sentence of Paragraph 32(5) of the KStG, that proof of the foregoing must be provided in the form of a certificate from the foreign tax authorities does not apply to the reimbursement of tax on income from capital to resident companies. It is unsure whether those rules, which, according to it, constitute an interference with the free movement of capital, are justified in the light of Article 65(1)(a) TFEU and of the criteria established by the Court in, inter alia, the judgment of 8 November 2007, Amurta (C‑379/05, EU:C:2007:655).

22. In the second place, in the event that the abovementioned national rules are considered to be compatible with the free movement of capital, the referring court queries whether the requirement of proof imposed by the fifth sentence of Paragraph 32(5) of the KStG on companies resident abroad receiving dividends from ‘free-float shares’ complies with the principles of proportionality and effectiveness where, as in the present case, it is practically impossible for those companies to provide such proof.

23. In those circumstances, the referring court decided to stay the proceedings and to refer the following questions to the Court of Justice for a preliminary ruling:

‘(1) Does Article 63 TFEU (ex Article 56 EC) preclude a national tax provision, such as that at issue in the main proceedings, which, for the purposes of the reimbursement of tax on income from capital, requires a company resident abroad which receives dividends from equity holdings and does not meet the minimum equity holding threshold laid down in Article 3(1)(a) of [Directive 90/435] to prove, by means of a certificate from the foreign tax administration, not only that neither that company nor a shareholder with a direct or indirect equity holding in that company can offset the tax on income from capital or deduct it as an operating cost or as work-related outgoings, but also that no offset, deduction or carry-forward has actually taken place either, in the case where such proof is not required, for the purposes of the reimbursement of tax on income from capital, from a company with the same level of equity holding which is resident in national territory?

(2) In the event that the answer to the first question is in the negative:

Do the principles of proportionality and effectiveness preclude the requirement of a certificate as referred to in the first question in the case where it is effectively impossible for a company in receipt of dividends from so-called “free-float” shares which is resident abroad to provide such a certificate?’

24. Written observations were submitted by ACC Silicones, the German Government and the European Commission.

The conclusion of the Advocate General

The Advocate General proposes that the Court should answer the first question referred for a preliminary ruling by the Finanzgericht Köln (Finance Court, Cologne, Germany) as follows:

Article 63 TFEU precludes a national tax provision, such as that at issue in the main proceedings, which, for the purposes of the reimbursement of tax on income from capital, requires a non-resident company which receives dividends from equity holdings and does not meet the minimum equity holding threshold laid down in Article 3(1)(a) of Council Directive 90/435/EEC of 23 July 1990 on the common system of taxation applicable in the case of parent companies and subsidiaries of different Member States, as amended by Council Directive 2003/123/EC of 22 December 2003, to prove, by means of a certificate from the foreign tax administration, that the tax cannot be offset by a shareholder with a direct or indirect equity holding in that company or be deducted by the latter company or by a shareholder with a direct or indirect equity holding in it as an operating cost or as work-related outgoings in the State of residence, in the case where such proof is not required, for the purposes of the reimbursement of tax on income from capital, from a company with the same level of equity holding which is resident in national territory. In order to be compatible with Article 63 TFEU, such a national provision must reimburse the tax on income from capital to the recipient non-resident company to the extent that the tax cannot be offset in the State of residence pursuant to any applicable convention for the avoidance of double taxation. Where only partial set-off is possible in the State of residence, the source State must reimburse the difference.

From the assessment of the Advocate General

A. Admissibility of the questions referred

25. In its written observations, the German Government submits that the questions put by the referring court also include companies whose registered office and/or centre of effective management is located in a third State. To that extent, those questions bear no relation to the facts of the main proceedings, which are limited to the tax treatment of dividends distributed to a company established in another Member State, and should thus be rejected as inadmissible.

26. According to settled case-law, in the context of the cooperation between the Court and the national courts provided for in Article 267 TFEU, it is solely for the national court before which the dispute has been brought, and which must assume responsibility for the subsequent judicial decision, to determine, in the light of the particular circumstances of the case, both the need for a preliminary ruling in order to enable it to deliver judgment and the relevance of the questions which it submits to the Court. Consequently, where the questions submitted concern the interpretation of EU law, the Court is in principle bound to give a ruling (judgment of 26 March 2020, A.P. (Probation measures), C‑2/19, EU:C:2020:237, paragraph 25 and the case-law cited).

27. It follows that questions relating to EU law enjoy a presumption of relevance. The Court may refuse to rule on a question referred by a national court for a preliminary ruling only where it is quite obvious that the interpretation of EU law that is sought bears no relation to the actual facts of the main action or its purpose, where the problem is hypothetical, or where the Court does not have before it the factual or legal material necessary to give a useful answer to the questions submitted to it (judgment of 26 March 2020, A.P. (Probation measures), C‑2/19, EU:C:2020:237, paragraph 26 and the case-law cited).

28. In the present case, the national provisions which are the subject of the reference for a preliminary ruling apply to companies, within the meaning of Article 54 TFEU or Article 34 of the EEA Agreement, which have their registered office and centre of effective management within the territory of a Member State of the European Union or of the European Economic Area (EEA). Furthermore, it is apparent from the order for reference that the dispute in the main proceedings concerns the right of a company having its registered office and centre of effective management in the United Kingdom to obtain reimbursement of withheld tax on income from capital in respect of dividends from free-float shares which had been distributed to it at a period during which that State was a member of the European Union.

29. However, in its order for reference, the referring Court points out that the requirement that the registered office and centre of effective management of the creditor must be located within the territory of a Member State of the European Union or of the EEA infringes EU primary law. It concludes that ‘point 1 of the first sentence of Paragraph 32(5) of the KStG must, in order to remain valid, be interpreted as meaning that it also applies to companies having their registered office and/or centre of effective management in third countries’ and that ‘so far as concerns the case at issue, this means that the rule contained in Paragraph 32(5) of the [KStG] would be relevant even if [ACC Silicones’] centre of effective management were not in the United Kingdom’. In addition, as the German Government rightly points out, the questions before the Court refer in general terms to companies ‘resident abroad’. Similarly, the doubts raised by the referring court concern ‘foreign companies’ or ‘companies resident abroad’ in general and are thus not confined to companies established in a Member State of the European Union or of the EEA other than Germany.

30. In my view, the question as to whether, in the case of dividends distributed to companies established in a third country, the conditions laid down by the German legislation at issue for obtaining reimbursement of withheld tax on income from capital are contrary to the EU rules on free movement of capital bears no relation to the subject matter of the main proceedings and is therefore hypothetical. It follows that the answer to that question does not appear to be necessary for the resolution of the dispute before the referring court.

31. Admittedly, as the referring court points out in its order for reference, Article 63(1) TFEU prohibits restrictions on the movement of capital both between Member States and between Member States and third countries. However, as the German Government correctly points out, the case-law concerning restrictions on the exercise of the freedoms of movement within the European Union cannot be transposed in its entirety to movements of capital between Member States and third countries, since such movements take place in a different legal context (see judgment of 26 February 2019, X (Controlled companies established in third countries), C‑135/17, EU:C:2019:136, paragraph 90 and the case-law cited). That is the case, in particular, as regards the evidential requirements imposed on taxpayers established in a third country in order to benefit from a tax advantage (see, to that effect, judgment of 26 February 2019, X (Controlled companies established in third countries), C‑135/17, EU:C:2019:136, paragraphs 91 and 92 and the case-law cited).

32. Consequently, the questions referred are, in my view, inadmissible in so far as they concern the reimbursement of withholding tax on income from capital in respect of dividends from free-float shares distributed to companies whose registered office and/or centre of effective management is located in a third country.

B. Preliminary observations

33. As is apparent from the order for reference, dividends paid by companies established in Germany to companies resident in any Member State are subject to tax on income from capital, levied by way of a withholding tax. However, in the years at issue and until March 2013, in accordance with Paragraph 8b(1) of the KStG, dividends distributed to companies established in Germany were not taken into account in the calculation of those companies’ income. Those companies thus had the benefit of a tax credit in respect of that withholding tax.

34. The conditions whereby tax on income from capital in respect of dividends from free-float shares that has been withheld and paid may be reimbursed differ according to whether the free-float equity participation is held by a non-resident company or by a company resident in national territory.

35. In the case of a non-resident company, reimbursement of withholding tax is subject to a condition that neither the non-resident company nor a shareholder with a direct or indirect equity holding in it must have been able to offset the tax on income from capital, deduct it as an operating cost or as work-related outgoings or carry it forward in the place of its tax residence. The income creditor is required to submit certificates from the relevant foreign tax authorities stating that the German tax on income from capital cannot be offset, deducted or carried forward and that no set-off, deduction or carry-forward has actually taken place either, in respect of itself and of all of its direct or indirect shareholders.

36. In the case of a resident company, the withholding tax is offset in full against the corporation tax payable by it and, where appropriate, is reimbursed thereto. The set-off and reimbursement (if any) of the tax are subject only to the condition that the tax has been withheld and paid, proof of which is submitted by way of a simple administrative certificate. Although resident companies could have direct or indirect non-resident shareholders, German legislation does not impose on them the same requirements as those contained in point 5 of the second sentence of Paragraph 32(5) of the KStG.

37. It is therefore clear that, as the referring court observes, under the applicable German legislation, the reimbursement of withholding tax on income from capital in respect of dividends from free-float shares is subject to stricter conditions where the income creditor is a non-resident company than those applicable where the income creditor is a resident company.

C. First question

38. Like the Commission, it seems to me that, by its first question, the referring court primarily seeks to ascertain whether the German legislation at issue is compatible with the free movement of capital to the extent that it permits a refusal to reimburse tax on income from capital in respect of dividends from free-float shares to non-resident companies where those companies or a shareholder with a direct or indirect equity holding in them can offset that tax, deduct it as an operating cost or as work-related outgoings or carry it forward. That question is to be assessed in the light of the fact that resident companies that have an equivalent equity holding in another resident company are not subject to such a condition in order to obtain reimbursement of withheld tax on income from capital.

39. In my view, the issue raised by the first question, contrary to what its wording might suggest, goes not so much to an evidential requirement as to one of the substantive conditions to be met in order to obtain reimbursement of the tax withheld. That under the fifth sentence of Paragraph 32(5) of the KStG, non-resident companies must prove that the substantive condition laid down in point 5 of the second sentence of Paragraph 32(5) of the KStG is satisfied by submitting certificates from the various tax authorities concerned, whereas such proof is not required from resident companies, merely constitutes the application of that condition to non-resident companies. Were one to conclude that the substantive condition is incompatible with the free movement of capital, that conclusion would apply to the evidential requirement automatically. By contrast, if one concluded that the substantive condition is compatible with the free movement of capital, it would be necessary to assess whether that conclusion ought to apply to the evidential requirement and, if not, whether the possible justification for the restriction arising from that requirement satisfied the principle of proportionality. I propose to address that alternative scenario in the context of the second question referred by the referring court.

40. According to settled case-law of the Court, measures prohibited by Article 63(1) TFEU as restrictions on the movement of capital include those that are such as to discourage non-residents from making investments in a Member State or to discourage that Member State’s residents from making investments in other States (judgment of 30 April 2020, Société Générale, C‑565/18, EU:C:2020:318, paragraph 22 and the case-law cited).

41. In respect of shareholdings which, as in the present case, are not covered by Directive 90/435, it is for the Member States to determine whether, and to what extent, economic double taxation or a series of charges to tax on distributed profits is to be avoided and, for that purpose, to establish, either unilaterally or through double taxation conventions concluded with other Member States, procedures intended to prevent or mitigate such economic double taxation. That does not, of itself, permit Member States to impose measures that contravene the freedoms of movement guaranteed by the FEU Treaty (judgment of 20 October 2011, Commission v Germany, C‑284/09, EU:C:2011:670, paragraph 48 and the case-law cited).

42. Thus, in its judgment of 20 October 2011, Commission v Germany (C‑284/09, EU:C:2011:670), the Court had occasion to hold, in respect of shareholdings not covered by Directive 90/435, that national tax legislation that treats dividends differently, depending on whether they are distributed to non-resident or resident companies, with the result that those dividends are subject to higher taxation in the former case, without that difference of treatment being neutralised by means of conventions, constituted a restriction on the movement of capital prohibited by Article 63 TFEU.

43. In the present case, contrary to the submissions of the German Government, the German legislation at issue clearly treats dividends from free-float shares distributed to non-resident companies less favourably than those distributed to resident companies since, as observed in point 37 above, the right to reimbursement of withheld tax on income from capital in respect of those dividends is subject to stricter conditions where the creditor of the income is a non-resident company, as distinct from where it is a resident company.

44. I am of the view that such a difference in treatment is liable to discourage non-resident companies from investing in companies established in Germany, and is also such as to constitute an obstacle to the raising of capital by resident companies from companies established in other Member States (see, to that effect, judgment of 2 June 2016, Pensioenfonds Metaal en Techniek, C‑252/14, EU:C:2016:402, paragraph 28 and the case-law cited).

45. It must be examined, however, whether the restriction resulting from the German legislation at issue is capable of being justified under the provisions of the Treaty. In that respect, it should be recalled that, pursuant to Article 65(1)(a) TFEU, Article 63 TFEU is, nonetheless, without prejudice to the right of Member States to apply the relevant provisions of their tax law which distinguish between taxpayers who are not in the same situation with regard to their place of residence or the place where their capital is invested.

46. Article 65(1)(a) TFEU, which derogates from the fundamental principle of the free movement of capital, must be interpreted strictly. It should not be construed to mean that any national measure which differentiates between taxpayers according to where they reside or the State in which they invest their capital is automatically compatible with the FEU Treaty. The derogation in that provision is itself limited by Article 65(3) TFEU, which stipulates that the national provisions referred to in paragraph 1 of that article ‘shall not constitute a means of arbitrary discrimination or a disguised restriction on the free movement of capital and payments as defined in Article 63 [TFEU]’ (judgment of 21 June 2018, Fidelity Funds and Others, C‑480/16, EU:C:2018:480, paragraph 47 and the case-law cited).

47. A distinction must, therefore, be made between differences in treatment which are permitted under Article 65(1)(a) TFEU and discrimination which is prohibited by Article 65(3) TFEU. For the German legislation at issue to be capable of being regarded as compatible with the Treaty provisions on the free movement of capital, the difference in treatment resulting from that legislation must concern situations which are not objectively comparable or be justified by an overriding reason in the public interest (judgment of 30 April 2020, Société Générale, C‑565/18, EU:C:2020:318, paragraph 24).

48. In the present case, it must be ascertained whether, having regard to the aim of the German legislation at issue, which, according to the order for reference, is to avoid a series of charges to tax on dividends, companies in receipt of free-float dividends are in comparable situations depending on whether they reside in Germany or in another Member State.

49. Contrary to the submissions of the German Government, I concur with the referring court and the Commission that that is the case here.

50. It is true that, from the point of view of measures laid down by a Member State in order to prevent or mitigate the imposition of a series of charges to tax on, or the economic double taxation of, profits distributed by a resident company, resident companies receiving dividends are not necessarily in a situation which is comparable to that of companies receiving dividends which are resident in another Member State (judgment of 20 October 2011, Commission v Germany, C‑284/09, EU:C:2011:670, paragraph 55 and the case-law cited).

51. Nevertheless, as soon as a Member State, either unilaterally or by way of a convention, imposes a charge to tax on the income not only of resident companies but also of non-resident companies from dividends which they receive from a resident company, the situation of those non-resident companies becomes comparable to that of resident companies (judgment of 8 November 2007, Amurta, C‑379/05, EU:C:2007:655, paragraph 38 and the case-law cited).

52. In fact, it is solely because of the exercise by that State of its power of taxation that, irrespective of any taxation in another Member State, a risk of a series of charges to tax or economic double taxation may arise. In such a case, in order for non-resident companies receiving dividends not to be subject to a restriction on the free movement of capital prohibited in principle by Article 63 TFEU, the State in which the company making the distribution is resident is obliged to ensure that, under the procedures laid down by its national law in order to prevent or mitigate a series of liabilities to tax or economic double taxation, non-resident companies are subject to the same treatment as resident companies (judgment of 8 November 2007, Amurta, C‑379/05, EU:C:2007:655, paragraph 39 and the case-law cited).

53. In the present case, the Federal Republic of Germany chose to exercise its power of taxation over free-float dividends distributed both to resident companies and non-resident companies, by levying a tax on income from capital by way of a withholding tax. Non-resident companies in receipt of those dividends thus find themselves in a situation comparable to that of resident companies as regards the risk of a series of charges to tax on dividends distributed by resident companies, so that they cannot be treated differently from the latter (judgment of 20 October 2011, Commission v Germany, C‑284/09, EU:C:2011:670, paragraph 58 and the case-law cited).

54. In its written observations, the German Government relies on the Convention, under which the rate of the withholding tax is limited to 15% and that tax can be offset against the tax payable in the United Kingdom. It maintains that the German legislature was entitled, in the case of non-resident companies, to subject reimbursement of withheld tax on income from capital to the fact that those companies, or companies that have a direct or indirect equity holding in them, cannot already claim the tax in their State of residence, in order to prevent a risk of double deduction of that tax.

55. It is true that, according to the case-law, it cannot be excluded that a Member State may succeed in ensuring compliance with its obligations under the Treaty through the conclusion of a convention for the avoidance of double taxation with another Member State (judgment of 8 November 2007, Amurta, C‑379/05, EU:C:2007:655, paragraph 79 and the case-law cited).

56. However, to that end, the application of such a convention should allow full compensation for the effects of the difference in treatment under national legislation. The difference in treatment between dividends distributed to companies established in other Member States and those distributed to resident companies does not disappear unless the tax withheld at source under national legislation can be offset against the tax due in the other Member State in the full amount of the difference in treatment arising under the national legislation (judgment of 17 September 2015, Miljoen and Others, C‑10/14, C‑14/14 and C‑17/14, EU:C:2015:608, paragraph 79 and the case-law cited).

57. In the present case, it is apparent from the order for reference that, as the German Government argues, pursuant to the Convention, the rate of the tax charged on the free-float dividends distributed to ACC Silicones was limited to 15%, and the withholding tax levied in Germany can be offset against the tax payable in the United Kingdom. However, the set-off is limited to the United Kingdom tax ‘computed by reference to the same profits’ or income by reference to which the German tax is computed. Thus, it cannot be ruled out, as ACC Silicones rightly observes, that the full amount of the German tax on income from capital paid in Germany may not be neutralised, which does not satisfy the requirements laid down in the case-law cited in point 56 above. Such neutralisation takes place only in cases where the dividends from Germany are sufficiently taxed in the other Member State, which presupposes that the amount of the United Kingdom tax computed by reference to the dividends distributed is at least equal to the amount of the withholding tax levied in Germany (see, to that effect, judgments of 20 October 2011, Commission v Germany, C‑284/09, EU:C:2011:670, paragraphs 67 and 68, and of 17 September 2015, Miljoen and Others, C‑10/14, C‑14/14 and C‑17/14, EU:C:2015:608, paragraph 86). It is for the referring court to ascertain whether that is the case in the main proceedings.

58. In that regard, I would add that I share the view of the Commission that a possible set-off of the German tax on income from capital against the tax liability of the direct or indirect shareholders of ACC Silicones cannot be taken into account, at least if those shareholders are non-resident. Indeed, as already indicated in point 36 above, in the case of resident companies receiving free-float dividends, the German legislation subjects the set-off or reimbursement of the tax on income from capital to the sole condition that the tax has been withheld and paid, another possible set-off of the tax in the State of residence of the shareholders of those companies, which could be non-resident shareholders, not being taken into consideration.

59. In the same context, I also concur with the Commission that a mere deduction of the withheld tax on income from capital as an operating cost or as work-related outgoings by the non-resident company or by its direct or indirect shareholders, in their State of residence, would be insufficient to neutralise the restriction to the free movement of capital so identified. Thus, the Court has held that, although Belgian legislation allows the deduction, as an expense, of tax paid abroad from the taxable base of income before applying a tax rate of 25% to the net amount of the dividends received by a taxpayer established in Belgium, such a deduction does not entirely compensate for the effects of any restriction on the free movement of capital in the Member State from which the dividends were paid (judgment of 17 September 2015, Miljoen and Others, C‑10/14, C‑14/14 and C‑17/14, EU:C:2015:608, paragraph 83).

60. In its written observations, the German Government maintains that, in any case, the national provisions at issue are justified by overriding reasons in the public interest, namely, first, the balanced allocation between the Member States of the power to impose taxes and, second, the need to avoid that tax withheld at source be taken into account twice.

61. According to settled case-law of the Court, a restriction on the free movement of capital is permissible only if it is justified by overriding reasons in the public interest, if it is suitable for securing the attainment of the objective which it pursues and if it does not go beyond what is necessary in order to attain that objective (see, to that effect, judgments of 26 February 2019, X (Controlled companies established in third countries), C‑135/17, EU:C:2019:136, paragraph 70, and of 30 January 2020, Köln-Aktienfonds Deka, C‑156/17, EU:C:2020:51, paragraph 83 and the case-law cited).

62. In my opinion, neither of the two justifications put forward by the German Government are applicable in this case.

63. As regards the first justification, it must be recalled that the need to safeguard the balanced allocation between the Member States of the power to impose taxes is a ground capable of justifying a restriction on the free movement of capital, in particular, where the national measures in question are designed to prevent conduct capable of jeopardising the right of a Member State to exercise its powers of taxation in relation to activities carried out in its territory (see, to that effect, judgments of 10 February 2011, Haribo Lakritzen Hans Riegel and Österreichische Salinen, C‑436/08 and C‑437/08, EU:C:2011:61, paragraph 121, and of 10 April 2014, Emerging Markets Series of DFA Investment Trust Company, C‑190/12, EU:C:2014:249, paragraph 98).

64. However, where a Member State has chosen not to tax recipient companies established in its territory in respect of income of that kind, it cannot rely on the argument that there is a need to ensure a balanced allocation between the Member States of the power to tax in order to justify the taxation of recipient companies established in another Member State (see, to that effect, judgment of 20 October 2011, Commission v Germany, C‑284/09, EU:C:2011:670, paragraph 78 and the case-law cited).

65. In the present case, it is common ground that free-float dividends distributed by resident companies benefit from a complete neutralisation of the effects of the deduction at source (points 8, 33 and 36 above).

66. As regards the second justification, the German Government submits that the national provisions at issue aim at preventing the tax on income from capital levied on free-float dividends being taken into account twice by non-resident companies receiving them or by their direct or indirect shareholders, once through reimbursement by the German tax authorities and then again through set-off against their tax liability or deduction as an operating cost or as work-related outgoings in their State of residence.

67. In my view, such an aim might, in principle, be regarded as permissible. Indeed, in the absence of such provisions, cross-border situations would confer an unjustified advantage over comparable national situations, in which, according to the German Government, it is not possible to take alternative or additional account of withheld and paid tax on income from capital at the level of the direct or indirect shareholders of the resident company receiving free-float dividends.

68. That being so, it should be recalled that, according to the case-law of the Court, to be considered as appropriate for attaining the objective relied upon, a measure must genuinely reflect a concern to attain that objective in a consistent and systematic manner (see, to that effect, in relation to restrictions on the freedom of establishment, judgment of 14 November 2018, Memoria and Dall’Antonia, C‑342/17, EU:C:2018:906, paragraph 52 and the case-law cited).

69. In my view, the German provisions at issue are incapable of attaining the objective of avoiding the tax withheld at source being taken into account twice since those provisions pursue that goal in an inconsistent manner. As observed at point 36 above, in the case of resident companies, the reimbursement of withholding tax is not subject to conditions equivalent to those demanded of non-resident companies, even though it cannot be ruled out that resident companies might have non-resident direct or indirect shareholders governed by national laws that allow the levied tax to be taken into account at their own level. Thus, it is possible that that tax might be taken into account twice in the case of resident companies. The fact, relied on by the German Government, that, under German law, the levied withholding tax can be taken into account only at the level of the resident company receiving the dividends does not alter this analysis.

70. I am therefore of the view that the aim relating to the need to avoid that tax withheld at source be taken into account twice put forward by the German Government does not justify the restrictions on free movement of capital contained in the national legislation at issue in the main proceedings.

71. Accordingly, Article 63 TFEU precludes a national tax provision, such as that at issue in the main proceedings, which, for the purposes of the reimbursement of tax on income from capital, requires a non-resident company which receives free-float dividends to prove, by means of a certificate from the foreign tax administration, that the tax cannot be offset by a shareholder with a direct or indirect equity holding in that company or be deducted by the latter company or by a shareholder with a direct or indirect equity holding in it as an operating cost or as work-related outgoings in the State of residence, in the case where such proof is not required, for the purposes of the reimbursement of tax on income from capital, from a company with the same level of equity holding which is resident in national territory. In order to be compatible with Article 63 TFEU, such a national provision must reimburse the tax on income from capital to the recipient non-resident company to the extent that the tax cannot be offset in the State of residence pursuant to any applicable convention for the avoidance of double taxation. Where only partial set-off is possible in the State of residence, the source State must reimburse the difference.

D. Second question

72. By its second question, the referring court asks whether, in the event that the German provisions at issue are found to be compatible with the free movement of capital, the evidential requirement laid down in the fifth sentence of Paragraph 32(5) of the KStG complies with the principles of proportionality and effectiveness.

73. Given the answer I propose be given to the first question, there is no need to answer the second. However, in the interest of completeness and in view of the possibility that the Court might take a different view as regards the first question, I shall address it briefly by focusing on the principle of proportionality, which appears to be more relevant to the case at hand than that of effectiveness.

74. Furthermore, I think that the second question should be considered from a different angle. As I observed at point 39 above, the principle of proportionality arises primarily in relation to possible justifications for restrictions on the free movement of capital.

75. In that regard, it must be recalled that, according to the case-law of the Court, although it is inherent in the principle of the fiscal autonomy of Member States that they determine what is, according to their own national system, the evidence required in order to benefit from a tax advantage, the exercise of that fiscal autonomy must be carried out in accordance with the requirements of EU law, in particular those imposed by the Treaty provisions on the free movement of capital. (judgment of 30 June 2011, Meilicke and Others, C‑262/09, EU:C:2011:438, paragraphs 37 and 38).

76. It is also apparent from the case-law of the Court that Member State tax authorities are entitled to require the taxpayer to provide such proof as they may consider necessary in order to determine whether the conditions for a tax advantage provided for in the applicable legislation have been met and, consequently, whether to grant that advantage (judgment of 30 June 2011, Meilicke and Others, C‑262/09, EU:C:2011:438, paragraph 45 and the case-law cited). In that respect, the Court has already stated that the possible difficulties that may arise in determining the tax actually paid in another Member State cannot justify a restriction on the free movement of capital (judgment of 12 December 2006, Test Claimants in Class IV of the ACT Group Litigation, C‑374/04, EU:C:2006:773, paragraph 70).

77. I believe that a national provision, such as the fifth sentence of Paragraph 32(5) of the KStG, under which reimbursement of withheld tax on income from capital to a non-resident company is granted only following submission of a certificate from the foreign tax authorities stating that the tax cannot be offset, deducted or carried forward and that no set-off, deduction or carry-forward has actually taken place either, and that in respect of both that company and all direct or indirect shareholders, without affording any opportunity for the non-resident company to adduce alternative proofs, is likely to constitute a disguised restriction on the free movement of capital prohibited by Article 65(3) TFEU (see, to that effect, judgment of 30 June 2011, Meilicke and Others, C‑262/09, EU:C:2011:438, paragraph 40 and the case-law cited).

78. It is true that a restriction on the free movement of capital may be justified by an overriding reason in the public interest. However, for such a restriction to be justified, it must observe the principle of proportionality, in that it must be appropriate for securing the attainment of the objective it pursues and must not go beyond what is necessary to attain it (judgment of 30 June 2011, Meilicke and Others, C‑262/09, EU:C:2011:438, paragraph 42 and the case-law cited).

79. It is clear to me that the evidential requirement laid down in the fifth sentence of Paragraph 32(5) of the KStG, to the extent that it concerns the direct and indirect shareholders of the non-resident company and that it excludes the possibility of providing alternative means of proof of the facts relied upon, is disproportionate in the light of the objectives put forward by the German Government. In that respect, I observe that, in its order for reference, the referring court states that ‘the requirement to prove that [the] condition [laid down in point 5 of the second sentence of Paragraph 32(5) of the KStG] is met in relation to all direct and indirect shareholders by submitting certificates to [that] effect from the foreign tax authorities … poses considerable difficulties for a taxable person seeking reimbursement of tax on income from capital’ and that ‘the production of those certificates sometimes necessitates a disproportionate amount of investigative effort or – as in the case at issue – can even be practically impossible’.

Copyright – internationaltaxplaza.info