On April 27, 2023 on the website of the Court of Justice of the European Union (CJEU) the judgment of the CJEU in Case C-537/20, L Fund versus Finanzamt D (in the presence of: Bundesministerium der Finanzen), ECLI:EU:C:2023:339, was published.

Introduction

This request for a preliminary ruling concerns the interpretation of Article 63 TFEU.

The request has been made in proceedings between L Fund and Finanzamt D (Tax Office D, Germany) concerning the liability of L Fund to corporate income tax for the financial years 2008 to 2010 (‘the tax years at issue’).

The dispute in the main proceedings, the question referred and the proceedings before the Court of Justice

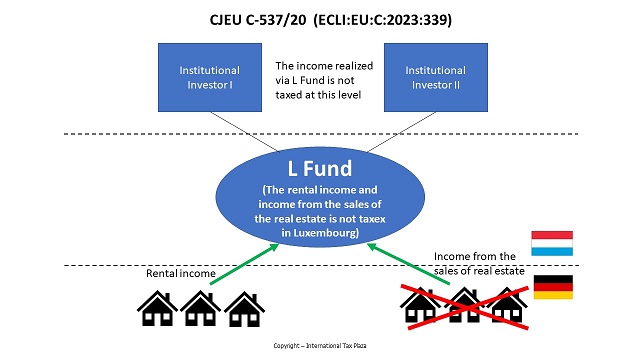

13 The applicant in the main proceedings, L Fund, is a property fund set up as a specialised investment fund under Luxembourg law, with neither its registered office nor its central administration in Germany.

14 L Fund is a closed-end fund with only two institutional investors and no head office or central administration in Germany.

15 Under Luxembourg law, as a specialised investment fund, L Fund is not taxable in Luxembourg, except for the tax on the raising of capital in civil and commercial companies and the subscription tax provided for in Paragraph 68 of the Law on specialised investment funds. By virtue of that right, dividends distributed by L Fund are not subject to withholding tax in Luxembourg and are not taxable at the level of non-resident investors.

16 During the tax years at issue, L Fund received income from the rental of its properties in Germany and from the sale of some of them.

17 In July 2013, it filed corporate income tax returns for the years at issue in respect of its partial liability to corporate income tax, but stated that, in its view, it was not liable for corporate income tax in Germany.

18 However, Tax Office D considered that L Fund was partially liable for corporate income tax and issued tax notices for the years at issue.

19 L Fund challenged those notices before the Finanzgericht Münster (Finance Court, Münster, Germany), which, by a judgment of 20 April 2017, confirmed, in essence, those notices.

20 L Fund lodged an appeal on a point of law against that judgment with the Bundesfinanzhof (Federal Finance Court, Germany) which is the referring court in the present case.

21 That court observes that, under Paragraph 2(1) of the KStG, L Fund, which has neither its registered office nor its central administration in Germany, is partially liable to corporation tax on the entire income which it received in that Member State. It does not benefit from any exemption of a personal or real nature. In contrast to domestic open-end investment funds, L Fund could not benefit from the exemption from corporate income tax provided for in the second sentence of Paragraph 11(1) of the InvStG 2004, since, under Paragraph 1(1)(2) of the InvStG 2004, read in conjunction with Paragraph 2(8) of the InvG in the version in force during the tax years at issue, L Fund is a foreign fund.

22 In that context, that court questions whether the exclusion of a foreign fund from the benefit of that exemption is compatible with EU law.

23 In that regard, while noting the existence of divergent positions, it indicates that, due to the specificities of German tax law, that exclusion could be compatible with Article 63 TFEU.

24 With regard to those specific features, the referring court explains that the exemption from corporate income tax of domestic funds under the second sentence of Paragraph 11(1) of the InvStG 2004 constitutes the implementation of the transparency principle, under which income is taxed only once, at the level of the investors. Pursuant to Paragraph 2(1) of the InvStG 2004, the latter must pay tax on dividends distributed to them or on income equivalent to such distribution in the case of a fund which retains the income it receives.

25 In the case of domestic specialised property funds with exclusively foreign investors, according to the second sentence of Paragraph 15(2) of the InvStG 2004, the income from property received by such a fund within German territory is attributed directly to the non-resident investors concerned as their own and partially taxable income. In order to ensure the taxation of the non-resident investors, the fund is obliged to levy a withholding tax under the fourth sentence of Paragraph 15(2) of the InvStG 2004.

26 The referring court states that the implementation of the transparency principle corresponds to the German legislature’s intention to prevent non-resident investors who, if they had invested directly in immovable property situated in the national territory, would have been partially liable to tax, from avoiding such liability to tax by making that investment through a specialised property fund. The transparency principle leads to non-resident investors being taxed as if they had made the direct investment.

27 By contrast, in the case of non-resident specialised property funds, income from property earned in Germany is taxable in the hands of the fund, which is liable to corporate income tax in so far as it does not benefit from the exemption provided for in the second sentence of Paragraph 11(1) of the InvStG 2004, whereas non-resident investors in the fund are not taxed, since the second sentence of Paragraph 15(2) of the InvStG 2004 applies only to domestic specialised property funds.

28 In both cases, income received in Germany by non-resident investors is thus taxed only once, but at different levels. That difference in tax treatment is due to the fact that, in the case of non-resident specialised property funds with non-resident investors, the German legislator cannot, on account of the principle of the territoriality of the public authority, guarantee, by means of a withholding tax, the right of the Federal Republic of Germany, as the Member State in whose territory the property in question is situated, to tax those non-resident investors.

29 Thus, in the present case, L Fund, as a foreign specialised property fund, would be subject to corporation tax on its income from property located in Germany, while its two non-resident institutional investors would not be taxable in that Member State.

30 By contrast, a comparable domestic specialised property fund with two non-resident institutional investors would not be subject to corporate income tax in Germany on such income due to the attribution of that income to those investors.

31 In the light of the foregoing, the referring court questions, in the first place, whether the exemption provided for in the second sentence of Paragraph 11(1) of the InvStG 2004 constitutes a restriction on capital movements within the meaning of Article 63(1) TFEU. First, that court doubts whether the exemption would deter non-resident investors from investing in German property, since the income from property derived therefrom would be taxed only once in the case of both resident and non-resident specialised property funds, but that taxation would be at different levels.

32 Secondly, it is also questionable whether that exemption has the effect of discouraging domestic investors from acquiring shares in non-resident specialised property funds. The double taxation resulting from the partial taxation of such funds under corporate income tax and the liability of such investors to capital gains tax on the dividends distributed by such funds would be largely eliminated by applying the deduction provided for in the seventh sentence of Paragraph 4(2) of the InvStG 2004. Moreover, if a specialised fund is used as an investment vehicle for a very limited circle of institutional investors for the purpose of investing in a specific object, the presence of potential domestic institutional investors could be seen as a purely hypothetical possibility.

33 In the second place, the referring court asks whether non-resident specialised property funds and domestic specialised property funds are in a comparable situation. According to that court, domestic specialised property funds with non-resident institutional investors are not subject to corporate income tax because of the direct allocation of income from property to non-resident investors under the second sentence of Paragraph 15(2) of the InvStG 2004, and the express partial liability of such income to corporate income tax, which shows that the national legislator used the tax status of the investors as a distinguishing criterion for determining the applicable tax treatment and that the taxation of the income from property is determined not at the level of the fund but according to the investors’ place of residence.

34 In the third place, the referring court questions whether the exemption of resident funds only under the second sentence of Paragraph 11(1) of the InvStG 2004 can be justified by overriding reasons in the public interest.

35 First, according to that court, the need to ensure a balanced distribution of the power of taxation between the Member States could be invoked to justify the exclusion of non-resident specialised property funds from that exemption, since taxation at the level of those funds of the income from property derived from immovable property situated in the territory of a Member State would make it possible to guarantee the right of taxation of that Member State in respect of that property, a right which cannot be guaranteed at the level of taxation of its non-resident investors.

36 Secondly, according to that court, the exclusion of L Fund from the benefit of that exemption could be justified by the need to preserve the coherence of the tax system, since that exemption for domestic specialised property funds is offset by the direct taxation of non-resident institutional investors in those funds under the second sentence of Paragraph 15(2) of the InvStG 2004.

37 In the fourth and last place, the referring court questions whether the refusal to grant the benefit of an exemption to non-resident specialised property funds goes beyond what is necessary in order to ensure the coherence of the German tax system for investments.

38 In those circumstances, the Bundesfinanzhof (Federal Finance Court) decided to stay the proceedings and to refer the following question to the Court of Justice for a preliminary ruling :

‘Does Article 56 [EC (now Article 63 TFEU)] conflict with a rule in a Member State, by virtue of which domestic specialised property funds with exclusively foreign investors are exempt from corporate income tax, while foreign specialised property funds with exclusively foreign investors are subject to limited liability for corporate income tax on their rental income obtained within the Member State?’

39 Following the service on that court of the judgment of 17 March 2022, AllianzGI-Fonds AEVN (C‑545/19, EU:C:2022:193), that court informed the Court of Justice, by a letter of 25 April 2022, that it wished to maintain its reference for a preliminary ruling.

Judgment

The CJEU (First Chamber) ruled as follows:

Article 63 TFEU must be interpreted as precluding legislation of a Member State which makes non-resident specialised property funds partially liable to corporate income tax in respect of the income from property which they receive in the territory of that Member State, whereas resident specialised property funds are exempted from that tax.

Legal context

German law

3 Paragraph 1(1)(5) of the Körperschaftsteuergesetz (Law on corporate income tax), in the version in force during the tax years at issue (‘the KStG’), provides:

‘Full liability

(1) The following legal persons, groups of persons and pools of securities whose central administration or registered office is located on the national territory are fully liable to corporate income tax:

…

(5) associations, institutions, foundations and other special purpose assets under private law without legal personality’.

4 Paragraph 2(1) of the KStG states:

‘Partial liability

The following are partially liable to corporate income tax:

(1) legal persons, groups of persons and pools of securities whose central administration and registered office are not located on the national territory, in respect of the income they receive on that territory’.

5 According to Paragraph 1 of the Investmentsteuergesetz 2004 (Law on investment tax 2004), in the version in force during the tax years at issue (‘the InvStG 2004’), entitled ‘Scope of application and definitions’:

‘This Law applies to:

(1) domestic collective investments, in so far as they are set up in the form of an investment fund within the meaning of Paragraph 2(1) of the Investmentgesetz [Law on investment (‘the InvG’)] or an investment company limited by shares within the meaning of Paragraph 2(5) [of the InvG] (domestic investment company), as well as the shares held in them (domestic shares in collective investments);

(2) foreign collective investments and the shares held in them within the meaning of Paragraph 2(8) and (9) [of the InvG].

…’

6 Paragraph 2(1) of the InvStG 2004, entitled ‘Income from shares’, provides:

‘Income distributed in respect of shares held in collective investments and income equivalent to such distribution as well as interim profit shall be deemed to be capital income within the meaning of Paragraph 20(1)(1) of the Einkommensteuergesetz [Law on Income Tax (‘the EStG’)] …’

7 Paragraph 4(2) of the InvStG 2004, entitled ‘Income received abroad’, states:

‘Where income distributed in respect of shares in collective investments and income equivalent to such distribution includes income from a foreign state which in that state is subject to a tax deductible from income tax or corporate income tax under Paragraph 34c(1) [of the EStG] or Paragraph 26(1) [of the KStG] or pursuant to a double taxation agreement, the amount of foreign tax determined and subsequently paid by the fully taxable investor, where no reduction is granted, shall be set off against that part of the income tax or corporate income tax which corresponds to such foreign income increased by the proportionate amount of foreign tax. … Where income distributed in respect of shares in foreign collective investments and income equivalent to such distribution includes income subject to capital gains tax in Germany, such income and the tax levied thereon in Germany shall be treated for the purposes of deduction thereof in the application of Paragraph 7(1) as foreign income and tax within the meaning of the first sentence. …’

8 Paragraph 7(1)(1) of the InvStG 2004, entitled ‘Capital Income Tax’, provides:

‘The following are liable to withholding tax on capital income:

(1) distributed income within the meaning of Paragraph 2(1) …’

9 Paragraph 11(1) of the InvStG 2004, entitled ‘Earmarked assets, tax exemption and tax audit’, states:

‘Statutory open-ended domestic collective investment schemes shall be deemed to be special-purpose assets within the meaning of Paragraph 1(1)(5) [of the KStG]. They shall be exempt from corporate income tax and trade tax. The second sentence shall also apply to investment companies. …’

10 Paragraph 15(2) of the InvStG 2004, entitled ‘Domestic specialised open-ended statutory collective investment schemes’, provides:

‘Income from the letting and management of immovable property and rights in rem assimilated to immovable property situated within the national territory, as well as profits from private sales transactions involving such property and rights, shall be accounted for separately. Such income shall be treated as income received directly by the partly taxable investor within the meaning of Paragraph 49(1)(2)(f), Paragraph 49(1)(6) or Paragraph 49(1)(8) [of the EStG]. The same applies to the application of the provisions of conventions for the avoidance of double taxation. Paragraph 7 shall apply, mutatis mutandis, with a tax rate of 25% of the income and a withholding of the tax on capital income by the investment company. …’

11 Paragraph 2(8) and (9) of the InvG, in the version in force during the tax years at issue, is worded as follows:

‘(8) Foreign collective investments are collective investments within the meaning of the second sentence of Paragraph 1, governed by the law of another State. They shall be deemed to comply with the principle of risk-spreading even if they consist to a significant extent of shares in one or more other investments and those other investments are invested directly or indirectly in accordance with that principle.

(9) Shares in foreign collective investment schemes are shares in foreign collective investment schemes issued by an enterprise located abroad (foreign investment company), which the investor may demand to be repaid in exchange for their return, or which he may not demand to be repurchased, the foreign investment company being in this case subject to prudential supervision of the assets intended for the collective investment scheme in the state in which its registered office is located.’

Luxembourg law

12 The law of 13 February 2007 on specialised investment funds (Mémorial A 2007, No 13) provides, in Paragraph 66(1), that ‘other than the capital duty levied on the raising of capital in civil and commercial companies and the subscription tax referred to in Paragraph 68 [of this law], no other tax shall be payable by the specialised investment funds referred to in this law’.

From the considerations of the Court

The question referred for a preliminary ruling

40 By its question, the referring court asks, in essence, whether Article 63 TFEU must be interpreted as precluding legislation of a Member State which makes non-resident specialised property funds partially liable to corporate income tax in respect of the income from property which they receive in the territory of that Member State, while resident specialised property funds are exempted from that tax.

41 According to the Court’s case-law, the Member States must exercise their competence in the field of direct taxation in compliance with EU law and, in particular, with the fundamental freedoms guaranteed by the TFEU (judgment of 29 April 2021, Veronsaajien oikeudenvalvontayksikkö (Income paid by UCITS), C‑480/19, EU:C:2021:334, paragraph 25).

42 Article 63(1) TFEU generally prohibits restrictions on movements of capital between Member States. The measures prohibited by that provision as restrictions on the movement of capital include those which are liable to dissuade non-residents from making investments in a Member State or to dissuade residents of that Member State from making investments in other States (judgment of 29 April 2021, Veronsaajien oikeudenvalvontayksikkö (Income paid by UCITS), C‑480/19, EU:C:2021:334, paragraph 26).

43 That being so, by virtue of Article 65(1)(a) TFEU, Article 63 TFEU is without prejudice to the right of Member States to apply the relevant provisions of their tax law which distinguish between taxpayers who are not in the same situation with regard to their residence or the place where their capital is invested.

44 That provision, in so far as it constitutes a derogation from the fundamental principle of the free movement of capital, must be interpreted strictly. Therefore, it cannot be interpreted as meaning that any tax legislation which makes a distinction between taxpayers on the basis of their place of residence or the State in which they invest their capital is automatically compatible with the TFEU. The derogation provided for in Article 65(1)(a) TFEU is itself limited by Article 65(3) TFEU, which provides that the national provisions referred to in paragraph 1 of that article ‘shall not constitute a means of arbitrary discrimination or a disguised restriction on the free movement of capital and payments as defined in Article 63 [TFEU]’ (judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 41 and case-law cited).

45 The Court also held that a distinction must therefore be drawn between differences in treatment permitted under Article 65(1)(a) TFEU and discrimination prohibited by Article 65(3) TFEU. For national tax legislation to be considered compatible with the provisions of the TFEU relating to the free movement of capital, the resulting difference in treatment must relate to situations which are not objectively comparable or be justified by an overriding reason relating to the public interest (judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 42 and the case-law cited).

46 It is therefore necessary to examine, first of all, the existence of a difference in treatment, next, the possible comparability of the situations, and finally, if necessary, the possibility of justifying the differential treatment.

The existence of a restriction on the free movement of capital

47 In the present case, it is apparent from the order for reference that, under the German legislation at issue in the main proceedings, resident specialised property funds are exempt from corporate income tax, whereas non-resident specialised property funds do not enjoy such an exemption.

48 Thus, non-resident and resident specialised property funds are subject to different treatment with regard to the taxation rules applicable to them, which is unfavourable to non-resident specialised property funds.

49 Such a difference in tax treatment is likely to dissuade, first, non-resident specialised property funds from making investments in property situated in Germany and, secondly, investors resident in Germany from using non-resident specialised property funds for such investments (see, to that effect, judgments of 10 May 2012, Santander Asset Management SGIIC and Others, C‑338/11 to C‑347/11, EU:C:2012:286, paragraph 17, and of 21 June 2018, Fidelity Funds and Others, C‑480/16, EU:C:2018:480, paragraph 44).

50 That conclusion cannot be called into question by taking into account the taxation applicable to dividends distributed to investors in resident specialised property funds, since the German legislation at issue in the main proceedings does not make the exemption of those funds subject to the condition that all of the income from property be taxed at the level of their investors.

51 In the case of non-resident specialised property funds with investors resident in Germany, it follows from that decision that, in addition to the partial liability of those funds to corporate income tax, those investors, who are fully liable to corporate income tax, are also liable to capital gains tax on the dividends distributed by the funds.

52 It is true that the deduction provided for in the seventh sentence of Paragraph 4(2) of the InvStG 2004 is intended to eliminate that double taxation. However, it appears from the case file that the complete elimination of such double taxation depends on the individual tax situation of each shareholder and is therefore uncertain. Moreover, the German Government stated at the hearing that, depending on their tax situation, resident investors in non-resident specialised property funds may be at a disadvantage compared to resident investors in resident specialised property funds.

53 In those circumstances, it must be held that legislation, such as the German legislation at issue in the main proceedings, constitutes a restriction on the free movement of capital prohibited, in principle, by Article 63 TFEU.

The comparability of the situations

54 It follows from the Court’s case-law, first, that the comparability or otherwise of a cross-border situation with a domestic situation must be examined having regard to the objective pursued by the national provisions at issue and to the purpose and content of those provisions, and, secondly, that only the relevant distinguishing criteria established by the legislation at issue must be taken into account for the purpose of assessing whether the difference in treatment resulting from such legislation reflects a difference in objective situation (judgment of 29 April 2021, Veronsaajien oikeudenvalvontayksikkö (Income paid by UCITS), C‑480/19, EU:C:2021:334, paragraph 49 and the case-law cited).

55 As regards the objectives pursued by the provisions of German law at issue in the main proceedings, it is apparent from the order for reference that the income from property of resident specialised property funds with non-resident institutional investors is taxed for corporate income tax purposes not at the level of the fund but at the level of the investors, in order to implement the transparency principle, under which income is taxed only once, and to ensure equality of treatment between direct investments and investments made through an investment fund. By taxing the income from property of resident funds only at the level of the investors, those provisions aim to avoid double taxation at the level of the fund and the investors.

56 It is also apparent from the documents before the Court that non-resident specialised property funds with non-resident investors are taxed at the level of the fund and not at the level of the investors, on the ground that, by reason of the principle of the territoriality of the public authority, the German legislature cannot guarantee, by means of a withholding tax, the right of the Federal Republic of Germany, as the Member State in whose territory the property in question is situated, to tax those non-resident investors.

57 In that regard, it is apparent from the documents before the Court that the only criterion of distinction established by the second sentence of Paragraph 11(1) of the InvStG 2004 is based on the place of residence of the funds, since only domestic funds benefit from the exemption from corporate income tax, investment funds governed by the law of another State being excluded from the benefit of that exemption. Similarly, the second sentence of Paragraph 15(2) of the InvStG 2004 applies only to resident specialised property funds.

58 It should be noted, first, that a non-resident specialised property fund may also have investors resident in Germany, on whose income the Federal Republic of Germany may exercise its power of taxation. From that point of view, a non-resident specialised property fund is in an objectively comparable situation to that of a resident specialised property fund (see, to that effect, judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 69 and the case-law cited).

59 Secondly, resident and non-resident funds are in a comparable situation with regard to the objective pursued by the transparency principle, namely to ensure equal treatment between direct investments and investments made through an investment fund. The income from property of resident funds is only taxed at the level of their investors for the purpose of achieving that objective.

60 Thirdly, the objective of shifting the level of taxation from the fund to the investor can also be achieved in the case of non-resident funds by making the exemption from corporate income tax provided for in the second sentence of Paragraph 11(1) of the InvStG 2004 conditional on the taxation of the investors of such funds. While the Federal Republic of Germany cannot tax non-resident investors, such an impossibility is consistent with the logic of shifting the level of taxation from the fund to the investor.

61 In those circumstances, it appears that reserving the possibility of obtaining an exemption from withholding tax solely to resident specialised property funds is not justified by an objective difference in situation between those funds and those resident in a Member State other than the Federal Republic of Germany (see, by analogy, judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 70 and the case-law cited).

62 Therefore, in the light of the objectives of the German legislation at issue in the main proceedings and the criterion of distinction established by that legislation, resident funds and non-resident funds are in a comparable situation.

63 Moreover, in the case giving rise to the judgment of 2 June 2016, Pensioenfonds Metaal en Techniek (C‑252/14, EU:C:2016:402), relied on by the German Government, the Court held that the differentiated treatment of the taxation of dividends paid to pension funds according to whether they were resident or non-resident, resulting from the application to those respective funds of two different methods of taxation, was justified by the difference in situation between those two categories of taxpayers in the light of the objective pursued by the national legislation at issue in that case and its purpose and content (judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU: C:2022:193, paragraph 51).

64 However, in that case, resident and non-resident funds, which were pension funds, were themselves taxed, but in a different way, given the objective of the national legislation at issue, which was, in the context of the retirement pensions system, to introduce neutral taxation, independent of the economic situation, of the various types of assets and all the forms of retirement savings concerned, since the State concerned could not guarantee that objective by taxing resident and non-resident funds in the same way.

65 In this case, resident funds are exempt from corporate income tax and are not subject to any other type of tax.

The existence of an overriding reason relating to the public interest

66 It should be noted that, according to the Court’s settled case-law, a restriction on the free movement of capital may be permitted if it is justified by overriding reasons relating to the public interest, is suitable for securing the attainment of the objective which it pursues and does not go beyond what is necessary in order to attain that objective (judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 75 and the case-law cited).

67 In the present case, the German Government argues in its written observations that, even if the German legislation at issue in the main proceedings constitutes a restriction on the free movement of capital, that restriction is justified in the light of two overriding reasons in the general interest, namely, first, the need to preserve the coherence of the national tax system and, secondly, the need to preserve a balanced distribution of taxing powers between the Member States.

The need to preserve the coherence of the national tax system

68 It should be noted that, while the Court has held that the need to preserve the coherence of a national tax system may justify national legislation of such a kind as to restrict the fundamental freedoms, it has made it clear that, in order for an argument based on such a justification to succeed, it must be established that there is a direct link between the tax advantage concerned and the offsetting of that advantage by a specific tax levy, the direct nature of that link having to be assessed in the light of the objective of the legislation in question (judgments of 16 December 2021, UBS Real Estate, C‑478/19 and C‑479/19, EU:C:2021:1015, paragraphs 65 and 66, and of 7 April 2022, Veronsaajien oikeudenvalvontayksikkö (Exemption for contractual investment funds), C‑342/20, EU:C:2022:276, paragraphs 91 and 92 and the case-law cited).

69 The referring court and the German Government consider that such a link exists, since the tax advantage of the exemption for resident funds is offset by the direct taxation of the non-resident institutional investors in those funds, since the second sentence of Paragraph 15(2) of the InvStG 2004 provides for the direct attribution of income from property to non-resident investors. In order to ensure the taxation of the latter, those funds would be obliged to levy a withholding tax under the fourth sentence of Paragraph 15(2) of the InvStG 2004. Furthermore, if the exemption under the second sentence of Paragraph 11(1) of the InvStG 2004 were to be taken into account, that exemption would be offset by the taxation of the investors under Paragraph 2(1) of the InvStG 2004, who would be subject to withholding tax under Paragraph 7 of the InvStG 2004.

70 In that regard, it must be noted that, although the exemption provided for in the second sentence of Paragraph 11(1) of the InvStG 2004 is not explicitly made subject, under that provision, to the condition that the taxation of the fund’s investors should make it possible to compensate for that exemption, such a direct link could nonetheless be inferred from the tax system at issue.

71 It is for the referring court, which alone has jurisdiction to interpret national law, to determine whether the direct attribution of income from property to non-resident investors and the taxation of resident investors in resident funds compensates for the exemption granted to those funds. In particular, it must determine whether such investors are systematically taxed and cannot benefit from an exemption from that tax.

72 Even supposing that such a direct link may derive from the tax system at issue, it is still necessary to ascertain whether, by reserving to resident specialised property funds alone the possibility of benefiting from income from property being exempted from corporate income tax, the legislation at issue in the main proceedings goes beyond what is necessary in order to ensure the coherence of that tax system (see, to that effect, judgment of 21 June 2018, Fidelity Funds and Others, C‑480/16, EU:C:2018:480, paragraph 83).

73 In that regard, it should be noted that in the case of resident investors in a non-resident specialised property fund, the taxation of that fund leads to double taxation of that income, since it is taxed, first, in the hands of the fund and, secondly, in the hands of the resident investor. As was pointed out in paragraphs 51 and 52 of the present judgment, the elimination of that double taxation cannot always be achieved, which is precisely the opposite of the objective pursued by the national legislation at issue in the main proceedings (see, to that effect, judgment of 21 June 2018, Fidelity Funds and Others, C‑480/16, EU:C:2018:480, paragraph 85).

74 Moreover, the internal consistency of the tax system at issue in the main proceedings could be maintained if non-resident specialised property funds could benefit from the exemption from corporate income tax, provided that the German tax authorities ensure, with the full cooperation of those funds, that the investors in those funds pay a tax equivalent to that to which investors in a resident specialised property fund are liable. Allowing such non-resident specialised property funds to benefit from that exemption, under those conditions, would constitute a less restrictive measure than the current regime (see, to that effect, judgment of 21 June 2018, Fidelity Funds and Others, C‑480/16, EU:C:2018:480, paragraph 84).

75 The need to preserve the coherence of the national tax system cannot therefore justify the restriction on the free movement of capital imposed by the German legislation at issue in the main proceedings.

The need to preserve a balanced distribution of taxing power between Member States

76 It should be noted that, as the Court has repeatedly held, the justification based on the preservation of the balanced allocation of the power to tax between the Member States may be accepted where the scheme at issue is intended to prevent conduct likely to jeopardise the right of a Member State to exercise its taxing powers in relation to activities carried out within its territory (judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 82 and the case-law cited).

77 However, where a Member State has chosen, as in the situation at issue in the main proceedings, not to tax resident funds on their domestic income, it cannot rely on the need to ensure a balanced allocation of the power of taxation between Member States in order to justify the taxation of non-resident funds which receive such income (see, by analogy, judgment of 17 March 2022, AllianzGI-Fonds AEVN, C‑545/19, EU:C:2022:193, paragraph 83 and the case-law cited).

78 It follows that the justification based on the preservation of a balanced allocation of the power to impose taxes between the Member States cannot be accepted either.

79 In the light of all of the foregoing considerations, the answer to the question referred is that Article 63 TFEU must be interpreted as precluding legislation of a Member State which makes non-resident specialised property funds partially liable to corporate income tax in respect of the income from property which they receive in the territory of that Member State, whereas resident specialised property funds are exempt from that tax.

Costs

80 Since these proceedings are, for the parties to the main proceedings, a step in the action pending before the referring court, the decision on costs is a matter for that court. Costs incurred in submitting observations to the Court, other than the costs of those parties, are not recoverable.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)