On March 28, 2024 on the website of the Dutch tax authorities a position paper of the Knowledge Group participation exemption answered the question what the amount of liquidation loss to be taken into account amounts to in the event of the dissolution and liquidation of a former sub-subsidiary (KG:023:2024:4). Prior to this dissolution and liquidation, this sub-subsidiary incurred a loss on the alienation of its subsidiary (a sub-sub-subsidiary of the taxpayer). Subsequently (direct) subsidiary of the taxpayer was dissolved and liquidated, as a result of which the shares of the (former) sub-subsidiary came into the possession of the taxpayer.

Facts

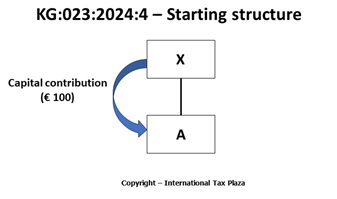

A taxpayer (X) incorporates a subsidiary (A) and contributes €100 of capital.

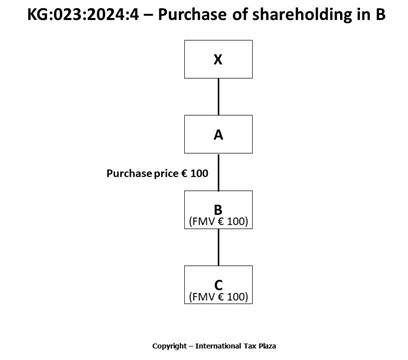

With this capital, A then acquires all shares in a sub-subsidiary (B) from non-related third parties against a purchase price of € 100. B, in its turn, holds all shares in a sub-sub-subsidiary of the taxpayer (C). The value of B, which amounts € 100, is entirely related to the shareholding in C.

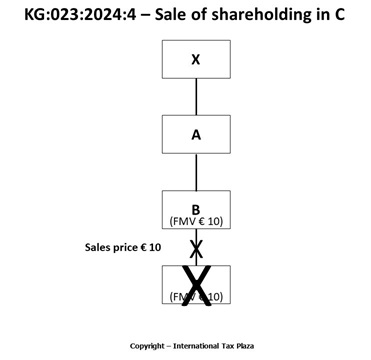

After several years B alienates all shares in C to a non-related third party for a sales price of € 10.

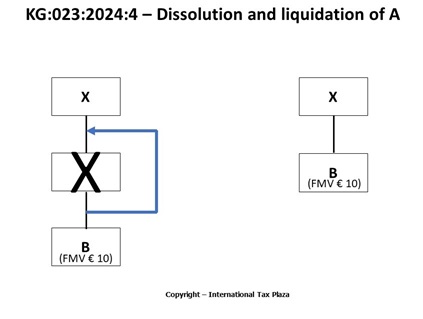

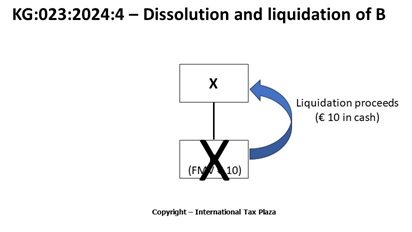

Later, A is dissolved and the liquidation is completed. The liquidation proceeds consists exclusively of the shareholding in B, of which the fair market value at that time amounts to € 10 (€ 10).

Shortly thereafter B was also dissolved and liquidated. The liquidation proceeds amount to € 10 fully consisting out of the cash that B received from the sale of C.

Question

What amount of liquidation loss, as referred to in Article 13d of the Dutch Corporate Income Tax Act (hereinafter: DCIT Act), can the taxpayer (X) take into account in the underlying case regarding the dissolution and completed liquidation of sub-subsidiary.

Legal context

Article 13d of the DCIT Act

For as far as relevant Article 13d of the DCIT Act reads as follows:

“(1) The participation exemption shall not apply to a loss on a participation that is expressed after the dissolution of the entity in which the taxpayer participates (liquidation loss).

(…)

(5) The liquidation loss is set at the amount by which the amount the taxpayer has sacrificed for the participation exceeds the total of the liquidation proceeds. (…)

(…)

(7) If, directly or indirectly, the assets of the dissolved body have included a shareholding which is part of the liquidation proceeds or which has been alienated and which has decreased in value since the acquisition of the participation in the dissolved entity, the liquidation loss shall only be taken into account to the extent that the loss exceeds the amount of said decrease in value. (…)

(…)

(9) (…) If a participation has been acquired from a related entity, the sacrificed amount at the time of the acquisition shall not exceed the amount that that entity has sacrificed for said participation. If such a participation has been acquired in the context of the dissolution of the related entity and the first sentence of Paragraph 7 has been applied to that participation, the sacrificed amount shall be increased by the decrease in value referred to therein up to the maximum sacrificed amount by the dissolved entity for that participation. (…)

(…)

(14) The liquidation loss shall only be taken into account at the moment that the liquidation is completed, provided that: (…).”

Answer as given by the Knowledge group

The liquidation loss to be taken into account by the taxpayer with respect to the dissolution and completed liquidation of B amounts to € 90, provided that the other conditions of the liquidation losses scheme are met. As a result of the application of Article 13, Paragraphs 7 and 9 of the DCIT Act, in the dissolution and liquidation of S the amount sacrificed for B amounts to € 100. The liquidation proceeds at the dissolution and liquidation of B amount to € 10, resulting in a liquidation loss of € 90.

At the dissolution and liquidation of B, Article 13d, Paragraph 7 of the DCIT Act is not applicable, since the decrease in value of C occurred before B was acquired by the taxable person.

The full text of the position paper (in Dutch) including the assessment of the tax Dutch authorities can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)