On December 21, 2023 on the website of the Dutch tax authorities a position paper of the Knowledge Group dividend withholding tax and withholding taxes of the Dutch tax authorities was published (KG:024:2023:24). In this position paper the Knowledge Group answers the question in which manner treaty benefits can be claimed with respect a share buyback if under the capital gains article of the applicable treaty for the avoidance of double taxation the levying rights over such buyback are not allocated to the Netherlands.

Facts

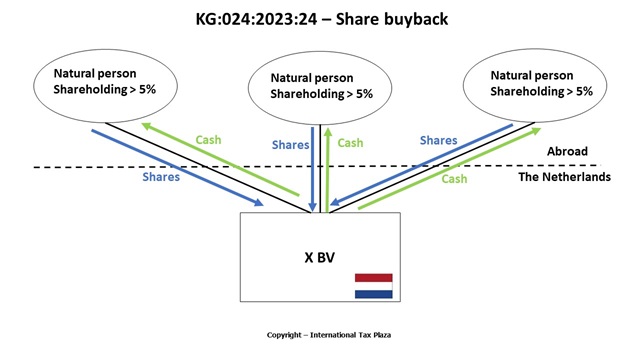

X BV buys back shares from a number of natural persons that have substantial interest in X BV as meant in Article 4.6 of the Dutch individual income tax (DIT) Act (aanmerkelijk belang) and that are residents of another State. Based on Article 3, Paragraph 1 of the Dutch dividend withholding tax (DDWT) Act X BV withholds Dutch dividend withholding tax with respect to the buyback. The capital gains article as included in the applicable treaty on the avoidance of double taxation however allocates the levying rights with respect to the share buy back to the other state (the state of which the shareholders are residents). Under the applicable treaty and accompanying protocol it is not the dividends article, but the capital gains article that applies to the buyback.

Question

How should the fact that under the capital gains article of a tax treaty the Netherlands does not have levying rights over the benefits of a share buyback be taken into account when levying Dutch dividend withholding tax?

Answer

If the capital gains article of that tax treaty does not allocate the levying rights over a share buyback to the Netherlands, then the distributing company does not have to withhold Dutch dividend withholding tax. No permit is required in this respect. In case Dutch dividend withholding tax has been withheld, a contest can be lodged with the Dutch tax authorities or if the period in which a contest can be lodged has expired a request for an official reduction can be submitted to the Dutch tax authorities.

The full (Dutch) text of the position paper including the legal assessment from the Dutch tax authorities, as published on the website of the Dutch tax authorities, can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)