Introductory remarks

For calculating the net qualifying income or loss of the constituent entities in a jurisdiction for a certain fiscal year you have to start by calculating the net qualifying income or loss of each separate constituent entity located in that jurisdiction for that fiscal year. And then adding together all these net qualifying incomes or losses of the constituent entities that are located in the same jurisdiction.

The net qualifying income or loss of the constituent entity is calculated by taking the financial accounting income or loss of a constituent entity and adjusting it in accordance with the rules defined in Chapter III (Calculation of the Qualifying Income or Loss) and in Chapters VI (Special Rules for Mergers and Acquisitions) and VII (Tax Neutrality and Distribution Regimes) of the proposed EU Directive.

Chapter III Calculation of the Qualifying Income or Loss

Chapter III contains rules for the determination of ‘qualifying income’, i.e. the adjusted income that will be taken into account for computing the effective tax rate (See Step 6). In order to compute this income, we start with the financial accounting net income or loss of the constituent entity for the fiscal year, as determined for the purpose of preparing consolidated financial statements. Then adjustments as defined in Article 15 of the proposed Directive are made to this income or loss.

In line with the OECD Model Rules, the Directive excludes international shipping income and partly ancillary international shipping income from the application of the GloBE Model Rules. This exclusion follows the principle whereby in national tax systems, income from shipping is often taxed pursuant to a separate set of rules from those of the mainstream corporate tax system.

This Chapter also includes rules specific to constituent entities that are a Permanent Establishment or a flow-through entity. In these cases, special rules are needed in order to avoid double counting or no counting of the income attributable to these entities. These special rules will also limit tax avoidance opportunities.

Chapter VI Special Rules for Mergers and Acquisitions

This chapter contains special rules in respect of mergers, acquisitions, joint ventures, and multi-parented MNE groups. It provides for the application of a consolidated revenue threshold to group members in a merger or demerger situation. When a constituent entity is acquired or sold by an MNE group within the scope of the rules, such a constituent entity should be treated as part of both groups during the year, with certain adjustments to the values of the attributes used for the operation of the GloBE Model Rules (covered taxes, eligible payroll, eligible tangible assets, GloBE deferred tax assets). There are rules for the recognition of a gain or loss, and carrying values in a transfer of assets and liabilities, including reorganisations. There is a special provision to include joint ventures, which would otherwise not be included in the definition of an MNE group for the GloBE purposes. Finally, there is a specific rule for multi-parented MNE groups in a way that group entities are treated as part of a single MNE group.

Chapter VII Tax Neutrality and Distribution Regimes

Chapter VII contains rules in respect of tax neutrality regimes and distribution tax systems.

In order to avoid unintended outcomes, such as a disproportionate UTPR top-up tax liability in an MNE Group, the Directive provides for special rules for the computation of the income of the ultimate parent entity, where such an entity is a flow-through entity or subject to a deductible dividend regime.

In respect of investment entities, there are specific rules for the determination of the ETR, the top-up tax, an election to treat them as tax transparent entities, and an election to apply a taxable distribution method.

In relation to distribution tax systems, the Directive provides that, on an annual election by the filing entity with respect to constituent entities which are subject to an eligible distribution tax system, a deemed distribution tax is included in the calculation of the adjusted covered taxes of the relevant constituent entities. This involves maintaining a deemed distribution tax recapture account for each fiscal year for which the election is made. If, in a four-year period, no tax is paid at the minimum rate on such deemed distribution, and the constituent entity has not incurred an allowable loss, then the top-up tax is payable based on the outstanding balance of the recapture account for the year in question.

Starting the actual calculation

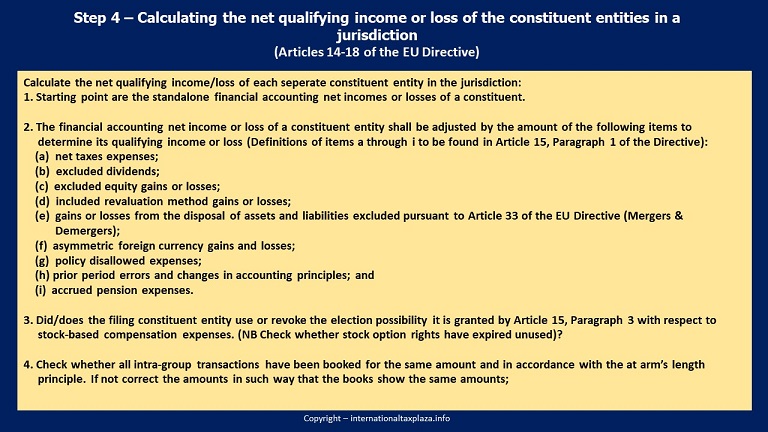

The standalone financial accounting net income or loss of a constituent entity is the starting point for the calculation its of qualifying net income or loss for the fiscal year. Standalone means: before any consolidation adjustments for intra-group transactions, as determined under the accounting standard used in the preparation of the consolidated financial statements of the ultimate parent entity.

Permanent Establishment

Article 17, Paragraph 1 of the Directive arranges that where a constituent entity is a permanent establishment as defined in Article 3, point 10, (a), (b) or (c) of the EU Directive, its financial accounting net income or loss shall be the net income or loss reflected in its separate financial accounts and where a permanent establishment does not have separate financial accounts, its financial accounting net income or loss shall be the amount that would have been reflected in its separate financial accounts if they had been prepared on a standalone basis.

Article 17, Paragraph 3 of the Directive arranges that where a constituent entity meets the definition of a permanent establishment in Article 3, point 10 (d) of the Directive, its financial accounting net income or loss shall be computed based on the items of income that are exempt in the jurisdiction where the main entity is located and attributable to the operations conducted outside of that jurisdiction and the items of expense that are not deductible for tax purposes in the jurisdiction where the main entity is located and that are attributable to such operations outside of that jurisdiction.

Article 17, Paragraph 4 of the Directive arranges that the financial accounting net income or loss of a permanent establishment shall not be taken into account in determining the qualifying income or loss of the main entity.

Adjustments to be made to the standalone financial accounting net income or loss of a constituent entity

The standalone financial accounting net income or loss of a constituent entity shall be adjusted by the amount of the following items to determine its qualifying income or loss:

(a) net taxes expenses;

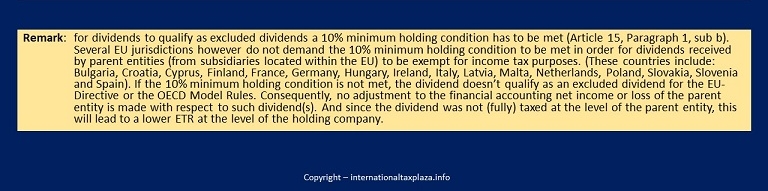

(b) excluded dividends;

(c) excluded equity gains or losses;

(d) included revaluation method gains or losses;

(e) gains or losses from the disposal of assets and liabilities excluded pursuant to Article 33 of the EU Directive;

(f) asymmetric foreign currency gains and losses;

(g) policy disallowed expenses;

(h) prior period errors and changes in accounting principles; and

Other items that might lead to an adjustment of the financial accounting net income or loss

Stock-based compensations

With respect to stock-based compensation expenses Article 15, Paragraph 3 of the Directive provides the filing constituent entity with possibility to elect that the amount of stock-based compensation expense that has been allowed as a deduction for tax purposes by a constituent entity for a fiscal year may be deducted from the financial accounting net income or loss of that constituent entity.

The election shall be made in accordance with Article 43, Paragraph 1 of the Directive and shall apply consistently to all constituent entities located in the same jurisdiction for the year in which the election is made and all subsequent fiscal years. In the fiscal year in which the election is revoked, the amount of unpaid stock-based compensation expense that exceeds the financial accounting expense accrued shall be included for the computation of the qualifying income or loss of the constituent entity.

Upon the unuse expiration of the stock options, the amount of stock-based compensation expense that has been deducted from the financial accounting net income or loss of the constituent entity for the computation of its qualifying income or loss for a fiscal year shall be added back in the fiscal year in which the option has expired.

Intra-group transactions

Transactions between constituent entities located in different jurisdictions shall be accrued for the same amount in the financial accounts of the constituent entities and for an amount consistent with the arm’s length principle.

A loss from a sale or other transfer of asset between constituent entities located in the same jurisdiction shall be accrued at an amount consistent with the arm’s length principle.

Refundable tax credits

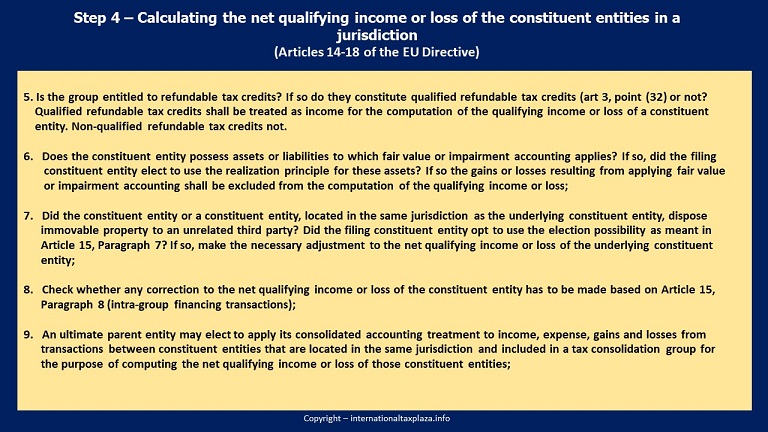

Qualified refundable tax credits shall be treated as income for the computation of the qualifying income or loss of a constituent entity. Refundable tax credits that do not meet the definition of a qualified refundable tax credit as set out in Article 3, point 32 of EU Directive shall not be treated as income for the computation of the qualifying income or loss of a constituent entity.

Gains & losses in respect of assets and liabilities subject to fair value or impairment accounting

Article 15, Paragraph 6 of the Directive arranges that at the election by the filing constituent entity, gains and losses in respect of assets and liabilities that are subject to fair value or impairment accounting in the consolidated financial statements of a constituent entity for a fiscal year may be determined on the basis of the realisation principle for the computation of the qualifying income or loss of that constituent entity for the same fiscal year.

In that case gains or losses which result from applying fair value or impairment accounting in respect of an asset or a liability shall be excluded from the computation of the qualifying income or loss of a constituent entity.

Disposal of immovable property

Article 15, Paragraph 7 of the EU Directive provides the filing constituent entity with the possibility to elect for offsetting a gain realized by a constituent entity on a disposal of immovable property (located in the same jurisdiction as in which the constituent entity is located) to third parties against any net loss arising from the disposal of immovable property in the fiscal year in which the election is made and in the four fiscal years prior to that fiscal year (the “five-year period”). Furthermore the paragraph contains regulations/conditions under which a residual amount of net gain can be allocated equally to the constituent entities located in that jurisdiction. The election has to be made annually.

Intra-group financing arrangements

If the conditions as laid down in Article 15, Paragraph 8 of the EU Directive are met, expenses related to a financing arrangement whereby one or more members of an MNE group provide credit to one or more other members of the same group (the “intra-group financing arrangement”) shall not be taken into consideration in the computation of the qualifying income or loss of a constituent entity.

An UPE electing to apply its consolidated accounting treatment to income, expense, gains and losses from intra-group transactions

Article 15, Paragraph 9 of the Directive arranges that an ultimate parent entity may elect to apply its consolidated accounting treatment to income, expense, gains and losses from transactions between constituent entities that are located in the same jurisdiction and included in a tax consolidation group for the purpose of computing the net qualifying income or loss of those constituent entities.

Insurance companies

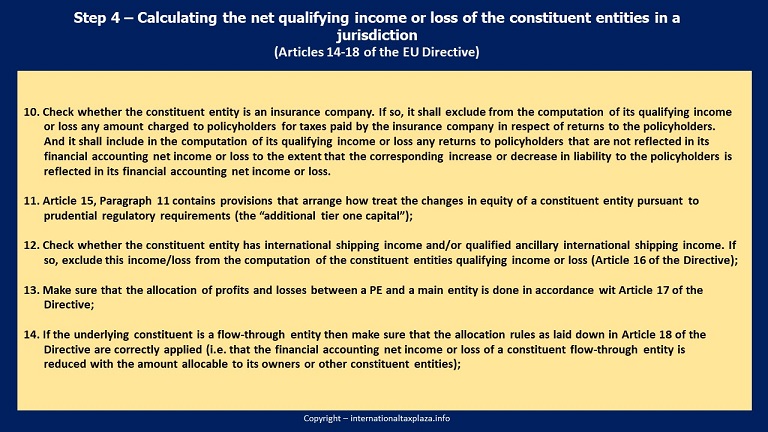

Article 15, Paragraph 10 of the Directive arranges that an insurance company shall exclude from the computation of its qualifying income or loss any amount charged to policyholders for taxes paid by the insurance company in respect of returns to the policyholders and that it shall include in the computation of its qualifying income or loss any returns to policyholders that are not reflected in its financial accounting net income or loss to the extent that the corresponding increase or decrease in liability to the policyholders is reflected in its financial accounting net income or loss.

Additional tier one capital

Article 15, Paragraph 11 of the Directive arranges that an amount that is accrued as a decrease in the equity of a constituent entity and is the result of distributions made or due in respect of an instrument issued by that constituent entity pursuant to prudential regulatory requirements (the “additional tier one capital”) shall be treated as an expense in the computation of its qualifying income or loss.

Any amount that is recognised as an increase in the equity of a constituent entity and is the result of distributions received or due to be received in respect of an additional tier one capital held by the constituent entity shall be included in the computation of its qualifying income or loss.

International shipping income and qualified ancillary international shipping income

Article 16 of the Directive contains provisions regarding international shipping income and qualified ancillary international shipping income and arranges a.o.:

- That he international shipping income and qualified ancillary international shipping income of a constituent entity shall be excluded from the computation of its qualifying income or loss, provided that the constituent entity demonstrates that the strategic or commercial management of all ships concerned is effectively carried on from within the jurisdiction where the constituent entity is located.

- That where the computation of a constituent entity’s international shipping income and qualified ancillary international shipping income results in a loss, such loss shall be excluded from the computation of the constituent entity’s qualifying income or loss.

- That to the extent that the total qualified ancillary international shipping income of the constituent entities located in a jurisdiction exceeds 50% of their total international shipping income, the excess income shall be included in the computation of their qualifying income or loss.

Permanent Establishments

Article 17, Paragraph 2 of the Directive arranges that where a constituent entity meets the definition of a permanent establishment in Article 3, point 10 (a) or (b) of the Directive, its financial accounting net income or loss shall be adjusted to reflect only the items of income and expense that are attributable to it in accordance with the applicable tax treaty or domestic law of the jurisdiction where it is located, regardless of the amount of income subject to tax and the amount of deductible expenses in that jurisdiction. and that where a constituent entity meets the definition of a permanent establishment in Article 3, point 10 (c) of the Directive, its financial accounting net income or loss shall be adjusted to reflect only the items of income and expense that would have been attributable to it in accordance with Article 7 of the OECD Model Tax Convention (“Business profits”).

Article 17, Paragraph 5 of the Directive arranges that where a qualifying loss of a permanent establishment is treated as an expense of the main entity in the computation of its domestic taxable income and is not set off against the domestic taxable income of the permanent establishment and the main entity, such qualifying loss shall be treated as an expense of the main entity for the computation of its qualifying income or loss.

Article 17, Paragraph 5 of the Directive furthermore arranges that qualifying income that is subsequently earned by the permanent establishment shall, by way of derogation from paragraph 4, be treated as qualifying income of the main entity up to the amount of the qualifying loss that was previously treated as an expense of the main entity under the first subparagraph.

Flow-through entities

Article 18, Paragraph 1 of the Directive arranges that the financial accounting net income or loss of a constituent entity that is a flow-through entity shall be reduced by the amount allocable to its owners that are not part of the MNE group and that hold their ownership interest in such flow-through entity directly or through one or more tax transparent entities, unless:

(a) the flow-through entity is an ultimate parent entity; or

(b) the flow-through entity is held, directly or through one or more tax transparent entities, by an ultimate parent entity.

Article 18, Paragraph 2 subsequently arranges that the financial accounting net income or loss of a constituent entity that is a flow-through entity shall be reduced by the financial accounting net income or loss that is allocated to another constituent entity.

Article 18, Paragraph 3 subsequently arranges that where a flow-through entity wholly or partially carries out business through a permanent establishment, its financial accounting net income or loss which remains after applying paragraph 1 shall be allocated to that permanent establishment in accordance with Article 17.

Based on Article 18, Paragraph 4 where a tax transparent entity is not the ultimate parent entity, the financial accounting net income or loss of the flow-through entity which remains after applying Paragraph 3 shall be allocated to its constituent entity-owners in accordance with their ownership interests in the flow-through entity.

Article 18, Paragraph 5 arranges that where a reverse hybrid entity or a tax transparent entity is the ultimate parent entity, the financial accounting net income or loss of the flow-through entity which remains after applying paragraph 3 shall be allocated to the reverse hybrid entity or the tax transparent entity.

According to Article 18, Paragraph 6, Paragraphs 3, 4 and 5 shall be applied separately with respect to each ownership interest in the flow-through entity.

Constituent entities joining and leaving a MNE group

Article 32, Paragraph 3 of the EU Directive arranges that in the acquisition year, and in each succeeding fiscal year, the qualifying income or loss and adjusted covered taxes of the target shall be based on the historical carrying value of its assets and liabilities.

Based on Article 32, Paragraph 9 of the EU Directive, the acquisition or disposal of a controlling interest in a target shall be treated as an acquisition or disposal of assets and liabilities (See the next Paragraph) provided that the jurisdiction in which the target is located, or in the case of a tax transparent entity, the jurisdiction in which the assets are located, treats the acquisition or disposal of that controlling interest in the same, or in a similar manner, as an acquisition or disposal of assets and liabilities, and imposes a covered tax on the seller based on the difference between the tax basis and the consideration paid in exchange for the controlling interest or the fair value of the assets and liabilities.

Transfer of assets and liabilities

Based on Article 33, Paragraph 2 of the EU Directive a constituent entity that disposes of assets and liabilities (the “transferring entity”) shall include the gain or loss arising from such disposal in the computation of its qualifying income or loss. It furthermore arranges that a constituent entity that acquires assets and liabilities (the “acquiring entity”) shall determine its qualifying income or loss on the basis of its carrying value of the acquired assets and liabilities determined under the acceptable financial accounting standard of the ultimate parent entity.

Article 33, Paragraph 3 of the EU Directive arranges that by way of derogation from paragraph 2, where a disposal or acquisition of assets and liabilities is performed in the context of a reorganisation:

(a) the transferring entity shall exclude any gain or loss arising from such disposal from the computation of its qualifying income or loss; and

(b) the acquiring entity shall determine its qualifying income or loss on the basis of the carrying value of the acquired assets and liabilities upon transfer.

Paragraph 4 arranges that by way of derogation from paragraph 2 and 3, where the transfer of assets and liabilities is performed in the context of a reorganisation which results, for the transferring entity, in a taxable gain or loss:

(a) the transferring entity shall include gain or loss arising from such disposal in the computation of its qualifying income or loss up to the portion of the gain that is subject to tax or up to the portion of the loss that reduces the taxable basis in the jurisdiction of the transferring entity; and

(b) the acquiring entity shall determine its qualifying income or loss on the basis of the carrying value of the acquired assets and liabilities upon transfer reduced by the portion of the gain that is subject to tax or increased by the portion of the loss that reduces the taxable basis in the jurisdiction of the transferring entity.

Based on Paragraph 5, at the election of the filing constituent entity, where a constituent entity that is required or permitted to adjust the basis of its assets and the amount of its liabilities to fair value for tax purposes in the jurisdiction where it is located, such constituent entity may:

(a) include, in the computation of its qualifying income or loss, an amount of gain or loss in respect of each of its assets and liabilities, which shall be equal to the difference between the carrying value for financial accounting purposes of the asset or liability immediately before the date of the event that triggered the tax adjustment (the “triggering event”) and the fair value of the asset or liability immediately after the triggering event;

(b) use the fair value for financial accounting purposes of the asset or liability immediately after the triggering event to compute qualifying income or loss in the fiscal years following the triggering event;

(c) include the net total of the amounts determined under (a) in the computation of the qualifying income or loss either by including the net total amounts in the fiscal year of the triggering event or by including one fifth of the net total of these amounts in the fiscal year of the triggering event and in the four following fiscal years.

The amount determined pursuant to point (a) shall be adjusted by any taxable gain or loss from the transfer to compute the taxable income after the transfer under local rules, if any, arising in connection with the triggering event.

If the constituent entity leaves the MNE group in a fiscal year before the full amount determined pursuant to point (a) has been included in the computation of its qualifying income or loss, the remaining amount shall be included in that fiscal year.

With respect to Paragraph 5 again the question arises whether the use of the term MNE Group means that that the provisions laid down in this Paragraph will only apply to a MNE Group or whether these provisions also apply to pure domestic multi-parented groups. Again in my view Paragraph 5 should apply to both to MNE groups and to pure domestic groups.

Ultimate parent entity that is a flow-through entity

Based on Article 36, Paragraph 1 of the proposed EU Directive the qualifying income of a flow-through entity that is an ultimate parent entity shall be reduced, for the fiscal year, by the amount of qualifying income that is allocated to the holder of an ownership interest (the “ownership holder”) in the flow-through entity, provided that:

(a) the income is subject to tax within 12 months after the end of this fiscal year at a nominal rate that equals or exceeds the minimum tax rate; or

(b) it can be reasonably expected that the total amount of covered taxes and taxes paid by the ownership holder on the income equals or exceeds an amount equal to that income multiplied by the minimum tax rate.

Paragraph 4 subsequently arranges that the covered taxes of a flow-through entity that is an ultimate parent entity shall be reduced proportionally to the amount of qualifying income reduced in accordance with paragraph 1.

Based on the second paragraph of Article 36 the qualifying income of a flow-through entity that is an ultimate parent entity shall be reduced, for the fiscal year, by the amount of qualifying income that is allocated to the holder of an ownership interest in the flow-through entity provided that the ownership holder is:

(a) a natural person that is tax resident in the jurisdiction where the ultimate parent entity is located and holds ownership interests representing a right to 5 % or less of the profits and assets of the ultimate parent entity; or

(b) a governmental entity, an international organisation, a non-profit organisation or a pension fund other than a pension services entity that is tax resident in the jurisdiction where the ultimate parent entity is located and holds ownership interests representing a right to 5% or less of the profits and assets of the ultimate parent entity.

According to Paragraph 3 the qualifying loss of a flow-through entity that is an ultimate parent entity shall be reduced, for the fiscal year, by the amount of qualifying loss that is allocated to the ownership holder of an interest in the flow-through entity. However, this reduction shall not apply where the ownership holder is not allowed to use such loss for the computation of its taxable income in the jurisdiction where it is tax resident.

The above shall apply also to a permanent establishment through which a flow-through entity that is an ultimate parent entity wholly or partly carries out its business or through which the business of a tax transparent entity is wholly or partly carried out provided that the ultimate parent entity’s ownership interest in that tax transparent entity is held directly or through one or more tax transparent entities.

Ultimate parent entity subject to a deductible dividend regime

Article 37 of the proposed EU Directive lays down provisions that apply to situations in which an ultimate parent entity is subject to a deductible dividend regime.

Article 37, Paragraph 2 of the proposed EU Directive arranges that an ultimate parent entity of an MNE group that is subject to a deductible dividend regime shall reduce, up to zero, for the fiscal year, its qualifying income by the amount that it distributes as deductible dividend within 12 months after the end of the fiscal year, provided that:

(a) the dividend is subject to tax in the hands of the recipient for a taxable period that ends within 12 months after the end of the fiscal year at a nominal rate that equals or exceeds the minimum tax rate; or

(b) it can be reasonably expected that the total amount of covered taxes and taxes paid by the recipient on such dividend equals or exceeds the amount equal to that income multiplied by the minimum tax rate.

Based on Article 37, Paragraph 3 an ultimate parent entity of an MNE group that is subject to a deductible dividend regime shall also reduce, up to zero, for the fiscal year, its qualifying income by the amount that it distributes as deductible dividend within 12 months after the end of the fiscal year, provided that the recipient is:

(a) a natural person, and the dividend received is a patronage dividend from a supply cooperative;

(b) a natural person that is tax resident in the same jurisdiction where the ultimate parent entity is located and that holds ownership interests representing a right to 5% or less of the profits and assets of the ultimate parent entity; or

(c) a governmental entity, an international organisation, a non-profit organisation or a pension fund other than a pension services entity that is tax resident in the jurisdiction where the ultimate parent entity is located and that holds ownership interests representing a right to 5% or less of the profits and assets of the ultimate parent entity.

Article 37, Paragraph 5 arranges that where the ultimate parent entity holds an ownership interest in another constituent entity that is subject to a deductible dividend regime, directly or through one or more constituent entities, paragraphs 2 and 3 shall apply to any other constituent entity located in the jurisdiction of the ultimate parent entity that is subject to the deductible dividend regime, to the extent that its qualifying income is further distributed by the ultimate parent entity to recipients that meet the requirements set out in paragraph 2.

Adding together all the net qualifying incomes or losses constituent entities located in the same jurisdiction

Once you have completed all the steps above you have determined the net qualifying income or loss of a constituent entity. You repeat all the steps mentioned above for each of the in-scope constituent entities that you have identified in Step 3. Once you have determined the net qualifying incomes or losses of all constituent entities in the same jurisdiction you add all these net qualifying incomes or losses together to determine the total jurisdictional net qualifying income or loss. This you repeat for all jurisdictions. Once you have done this you move forward to Step 5, which is determining the adjusted covered taxes of the constituent entities in the jurisdiction.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter