In this article we discuss position paper KG:011:2022:9 of May 25, 2022. In this position paper the Knowledge Group special profit provisions for Dutch corporate income tax purposes of the Dutch tax authorities answers a question regarding a so-called Total Return on Equity Swap (TRES) and the application of Articles 10c and 25 of the Dutch Corporate Income Tax (DCIT) Act in that context.

Please note that at the same time the Knowledge Group on dividend withholding tax and other withholding taxes answers the question whether a Total Return on Equity Swap (TRES) qualifies as a share buy-back (of own shares) as meant in Article 3, Paragraph 1 under a of the Dutch dividend withholding tax (DDWT) Act. We already published article on that position paper on May 17, 2023. Our article from May 17, 2023 can be found here.

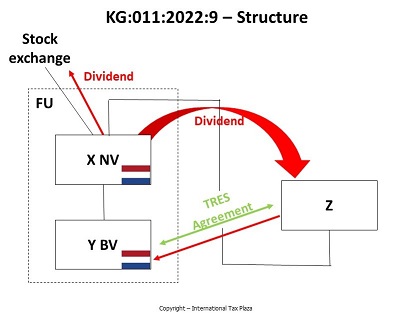

Facts of the underlying case

- X NV (a public limited liability company) is a listed company that is a resident of the Netherlands;

- Y BV is a subsidiary that is included in the fiscal unity for DCIT purposes of which X NV is the parent entity;

- X BV enters into the TRES on the shares of X NV;

- Y BV concludes the TRES with a foreign financial service provider, Z;

- A TRES generally results in three liabilities / cash flows. The TRES is a derivative whereby Y BV and Z agreed that during the term of the contract the increase in value of a certain number of shares in X NV, as well as the equivalent of net dividends paid on those shares, will be for the benefit of Y BV in return for which Y BV pays a periodic fee to Z. Any decrease in value in the shares in X NV will at the expense of Y BV;

- The periodic payment that the fiscal unity of X NV owes to Z consists of interest over an amount equaling the purchase price paid by Z for obtaining the underlying shares in X NV;

- Y BV did not enter into this TRES for the fulfillment of share or option obligations towards employees;

- The holder of the TRES is entitled to the monetary value of the increase in value of the agreed number of shares, but must compensate an amount equal to that decrease in value in the event of a decrease in value;

- In principle, the TRES has a fixed term and includes the option for early termination. An extension, whereby the parties again agree on the conditions, is also possible;

- Z buys the contractually agreed number of X NV shares in the market. Z is obliged to in any event possess the X NV shares in the period from the ex-dividend date to the dividend determination date (‘the record date’);

- In no way does the TRES oblige Z to transfer the shares in X NV to either X NV or Y BV; and

- At no moment in time will Z hold 5% or more of the nominal issued capital of X NV.

Questions

Question 1

Does Article 10c of the DCIT Act apply to the TRES at the level of the fiscal unity in a situation in which a subsidiary, that is included in the fiscal unity, enters into a TRES with financial service provider Z, in the context of which Z temporarily purchases shares in the parent company of the fiscal unity?

Question 2

Is the fiscal unity entitled under Article 25 of the DCIT Act to offset the dividend withholding tax withheld from the dividends paid out on the shares that were purchased by Z under the TRES?

Question 3

Are the fees that the subsidiary pays to Z for the TRES deductible for Dutch corporate income tax purposes at the level of the fiscal unity?

Legal context

Article 10c of the DCIT Act

Article 10c of the DCIT Act arranges that income realized on own shares and shares of an entity that has an interest of at least one third in the taxpayer will not be taken into account when determining the taxable profit of the taxpayer if these shares have been bought as a temporary portfolio investment. In this respect a right to acquire such a share as well as a right of which the value is directly or indirectly related to the change in value of such a share is equated with a share.

Article 25 of the DCIT Act

Article 25 arranges a.o. that dividend withholding tax that has been withheld on income sources that are part of the Dutch taxable profit and the Dutch taxable income of a taxpayer is considered to be a pre-levy for DCIT purposes. (NB exceptions exits) and that such dividend withholding tax withheld can be set off/deducted from the amount of Dutch corporate income tax due.

Answers

Question 1

Yes, Article 10c of the DCIT Act applies to the TRES.

Question 2

No. Pursuant to Article 25 of the DCIT Act there is no room for setting of dividend withholding tax against the Dutch corporate income tax purposes, since the fiscal unity cannot be regarded as the legal owner, nor as the other beneficiary of the proceeds nor is the fiscal unity directly entitled to the dividend. It therefore does not meet the so-called basis requirement of Article 25, Paragraph 1 of the DCIT Act.

Question 3

No. The fees paid for the TRES cannot be deducted from the profit, but as being part of the cost price of the TRES they reduce the benefit of the TRES that pursuant to Article 10c of the DCIT Act is not taken into account for Dutch corporate income tax purposes.

The full Dutch text of the position paper (in the Dutch language) with extensive considerations can be found here.

Other position pares on Dutch corporate income tax we already discussed earlier can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)